65% of Americans head toward retirement without a documented financial plan. But here’s what can change the game – a financial planner who uses specific retirement strategies can boost your retirement income by 22.6% each year.

My years of experience helping people direct their path to retirement success shows that proper planning creates the real difference. A 65-year-old couple needs approximately $315,000 just for healthcare expenses during retirement. The numbers tell us that 70% of Americans aged 65 and above will need long-term care eventually.

These 7 proven retirement planning strategies work effectively in 2025. The U.S. Department of Labor suggests maintaining 70-90% of your pre-retirement income. You might also want to take advantage of new opportunities like the increased 401(k) contribution limits of $23,500. These practical steps will secure your financial future.

Define Your Retirement Vision with Clarity and Purpose

Image Source: Upmetrics

“Retirement is wonderful if you have two essentials – much to live on and much to live for.” — Author Unknown, Anonymous

A clear vision of your dream retirement years is vital to successful planning. My experience helping clients plan their retirement shows that you need a practical approach to line up your values with real financial goals.

Identifying Your Core Retirement Values

Your personal values are the foundations of a rewarding retirement. Through my advisory career, I’ve seen how living by these core principles leads to retirement satisfaction. List the values that strike a chord with you and pick your top five most essential ones [1]. To name just one example, if philanthropy tops your list, make charitable giving a key part of your retirement plan. It also makes sense to set up scholarship funds or 529 plans for your grandchildren’s education if learning ranks high on your list [1].

Setting SMART Retirement Goals

SMART (Specific, Measurable, Attainable, Relevant, Timely) goals help turn your retirement dreams into reality. Rather than saying “I want to retire comfortably,” set a specific target like “I want to retire at 65 with $1.5 million saved” [2]. Retirement calculators help track your progress and let you adjust your strategy when needed [2].

Your retirement goals should include these key elements:

- Calculate required monthly savings

- Determine your ideal retirement age

- Estimate healthcare costs, which can reach $315,000 for a 65-year-old couple [3]

- Plan for inflation adjustments, currently at 2.5% for Social Security benefits [4]

Creating a Retirement Lifestyle Blueprint

Your retirement blueprint should cover both financial and lifestyle aspects. Note that living on your expected retirement budget before you retire helps confirm your plan’s feasibility [3]. Think about how you’ll spend time that was once dedicated to work [5].

The retirement transition wheel focuses on these key areas:

- Social connections and relationships

- Health and wellness activities

- Personal growth opportunities

- Meaningful community participation

- Financial security measures

Lining Up Financial Plans with Personal Aspirations

Clear values and lifestyle goals should shape your financial strategy. Dual-income households can maximize employer matching contributions by coordinating retirement accounts [6]. Partners should balance investment risks to create a unified approach that reflects both people’s retirement goals [6].

Longer life expectancies mean your financial strategy should include:

- Coordinating Social Security claiming strategies

- Balancing investment portfolios based on shared objectives

- Creating tax-efficient withdrawal plans

- Establishing emergency funds covering 3-6 months of non-discretionary expenses [7]

Retirement planning evolves with time. Review and update your blueprint yearly or when life throws major changes your way [1]. This flexible approach keeps your retirement strategy in sync with your changing values and goals.

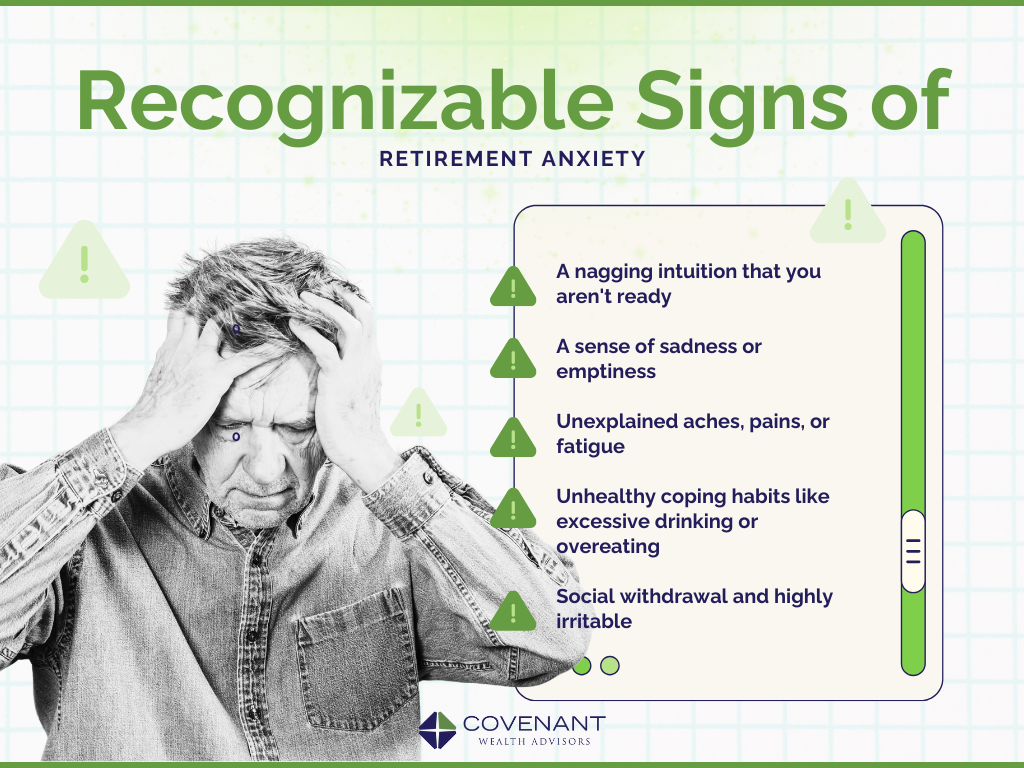

Master the Psychology of a Successful Retirement Transition

Image Source: Covenant Wealth Advisors

Financial preparation is the foundation of retirement planning, but knowing how to handle the psychological aspects of this life transition is equally significant. My experience as a financial advisor shows that emotional readiness affects retirement success by a lot.

Preparing for the Emotional Impact of Retirement

Retirement brings unexpected emotional challenges that many people aren’t ready to face. Studies reveal that 28% of retirees experience depression, which is nowhere near the rate in the general older population [8]. Retirement isn’t just a “permanent vacation” – it changes your sense of purpose and daily structure completely.

Retirees feel excited about their newfound freedom during the original “honeymoon phase.” All the same, this enthusiasm fades and leads to what experts call “retirement shock” [9]. You should start preparing emotionally at least two years before retirement. This gives you time to process upcoming changes and develop ways to cope.

Building New Identity Beyond Your Career

Reconstructing identity after leaving professional roles is one of retirement’s biggest challenges. Research shows people who define themselves only through their careers don’t deal very well with this transition [10]. Rather than seeing retirement as an ending, call it a new beginning – a chance to reinvent yourself.

Here’s how to build a reliable post-career identity:

- Explore interests outside work before retiring

- Develop new skills or adapt existing ones

- Consider part-time work or mentoring opportunities

- Focus on personal growth and learning

Maintaining Social Connections

Social connections matter more after retirement, especially since leaving work creates a social vacuum [11]. Studies show strong social networks can reduce cognitive decline and dementia risk by up to 70% [11]. Seniors with larger social networks show better cognitive abilities and increased brain volume [11].

You can strengthen your social network by:

- Staying connected with former colleagues

- Joining community groups or clubs

- Getting involved in volunteer activities

- Taking part in lifelong learning programs

Developing Healthy Financial Behaviors

Financial wellness goes beyond numbers – it’s about creating healthy money habits that bring peace of mind. Research shows 57% of households save for three or more goals [12].

The foundations of financial wellness include setting up a budget, managing cash flow, and building emergency funds [13]. Studies show people with higher financial literacy scores have better saving accumulations and make smarter long-term financial decisions [14].

Emotional stability plays a vital role in financial behavior. Research shows people in the lowest quintile of emotional stability have a 10% higher chance of experiencing financial distress [2]. People with high conscientiousness and emotional stability show only a 1% chance of facing financial difficulties [2].

Over the last several years of advising retirees, I’ve seen that successful transitions need both emotional and financial preparation. When you address these psychological aspects early, you’re more likely to achieve a retirement that matches your values and goals.

Construct a Resilient Retirement Income Foundation

Image Source: Western & Southern Financial Group

“Retirement is like a long vacation in Las Vegas. The goal is to enjoy it the fullest, but not so fully that you run out of money.” — Jonathan Clements, Financial Writer and Former Wall Street Journal Columnist

Building a strong retirement income foundation requires you to think over both guaranteed and variable income sources. My years of advising retirees have shown that creating green practices for retirement income needs a strategic mix of different income streams.

Creating Reliable Income Streams

A well-laid-out retirement income plan combines multiple sources to ensure financial stability. Social Security is the life-blood that provides inflation-adjusted benefits and maintains purchasing power throughout retirement [15]. Research shows that delaying Social Security claims until full retirement age (65-67) increases benefits by 20-30%. You can get an additional 8% boost for each year delayed until age 70 [16].

Pension plans and annuities provide dependable income streams beyond Social Security. My clients learn that Social Security adds to their retirement savings [17]. Broadening income sources becomes significant to ensure long-term financial security.

Balancing Guaranteed vs. Growth-Oriented Income

Success in retirement depends on the right balance between guaranteed and growth-oriented income. Fidelity’s retirement analysis uses a 2.5% inflation rate to assess retirement goals [15]. To curb this effect, you should maintain a diversified portfolio that has:

- Growth assets like U.S. and international stocks that can pass higher prices to customers

- Treasury Inflation-Protected Securities (TIPS) for inflation protection

- Commodity-linked investments that benefit from rising prices historically

Protecting Against Sequence of Returns Risk

Sequence of returns risk threatens retirement savings, especially in the early years. Research shows that withdrawals during market downturns can devastate retirement savings [18]. To reduce this risk, you should implement a bucket strategy:

- Short-term bucket (0-5 years): Safe, liquid assets for immediate expenses

- Mid-term bucket (5-10 years): Moderate-risk investments

- Long-term bucket (10+ years): Growth-oriented investments [19]

An emergency fund that covers 3-6 months of expenses helps protect against unexpected financial shocks [20].

Adjusting Income Plans for Inflation

Inflation worries many retirees. A modest 3% inflation rate over 20 years can reduce $100,000’s purchasing power to just $55,000 [1]. To protect against inflation’s effects, I support:

- Growth investments alongside conservative options

- Inflation-resistant investments within portfolios

- Strategic withdrawal rates

The traditional 4% rule provides a starting point, but flexibility remains essential. You should adjust withdrawal amounts during market volatility to preserve retirement savings [16]. Healthcare costs need special attention. A 65-year-old might need $165,000 in after-tax savings for medical expenses [15].

My experience shows that retirees who direct their retirement successfully take a balanced approach. They combine guaranteed income sources with growth-oriented investments and stay flexible enough to adjust strategies when needed. Retirement planning focuses on managing risks effectively to ensure lasting financial security.

Implement Strategic Tax Planning Across Retirement Phases

Image Source: Meld Financial

Tax planning is the life-blood of a successful retirement, but many retirees don’t realize how vital it is. My decades of helping clients direct their retirement journey shows how good tax planning can boost after-tax retirement income by a lot.

Pre-Retirement Tax Optimization

Good tax planning should start well before retirement. Your best move as retirement gets closer is to max out contributions to tax-deferred accounts like 401(k)s and traditional IRAs. These contributions lower your current taxable income [21]. You’ll need to balance traditional and Roth accounts carefully since your retirement tax bracket might end up higher than you expect.

Couples with two incomes should coordinate their retirement accounts to get the most from employer matching contributions. Living in or moving to a tax-friendly state can make a huge difference in your retirement savings. Right now, seven states don’t have state income tax: Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, and Wyoming [21].

Tax Diversification Strategies

Tax diversification helps you manage retirement income better. Having different accounts with varied tax treatments gives you more flexibility in retirement. Here are the three main types of accounts:

- Tax-deferred accounts (Traditional IRAs, 401(k)s)

- Tax-free accounts (Roth IRAs)

- Taxable investment accounts

Roth conversions offer another valuable option, especially if you think tax rates will be higher when you retire [22]. Just keep in mind that conversions create immediate tax bills, so timing matters.

Managing RMDs Effectively

Required Minimum Distributions (RMDs) now start at age 73 [21], which changes retirement planning quite a bit. Here are some smart ways to handle RMDs:

- Qualified Charitable Distributions (QCDs) let you transfer up to $108,000 directly from IRAs to charities in 2025. These count toward RMD requirements without raising your taxable income [23].

- Qualified Longevity Annuity Contracts (QLACs) allow you to invest up to $210,000 in 2025 from retirement accounts and delay RMDs until age 85 [24].

Missing RMDs leads to a big 25% penalty on amounts not withdrawn, though this drops to 10% if fixed within two years [25]. Setting up automatic RMD withdrawals helps avoid these costly mistakes.

Estate Tax Considerations for Heirs

Tax strategy and estate planning go hand in hand. Current law gives inherited investments in taxable accounts a “step-up” in cost basis, which makes gains during the original owner’s lifetime tax-free for heirs [26].

The SECURE Act of 2019 brought major changes to retirement account inheritance. Most non-spouse beneficiaries must now empty inherited retirement accounts within 10 years of the original owner’s death [26]. This shorter timeline might push heirs into higher tax brackets during the distribution period.

Here’s how to make things more tax-efficient for heirs:

- Pass on taxable assets to heirs for step-up benefits

- Give Roth accounts to higher-income beneficiaries

- Use charitable giving strategies with tax-deferred accounts

Smart tax planning throughout these stages can help you keep more wealth for both retirement and your heirs. Tax laws keep changing, so review and adjust your strategy regularly to stay successful long-term.

Design a Comprehensive Healthcare and Wellness Strategy

Image Source: Boomer Benefits

Healthcare costs rank among the biggest expenses you’ll face in retirement. You need a detailed strategy to ensure long-term financial security. My work with retirees has taught me that planning healthcare ahead of time makes the difference between retiring comfortably and struggling financially.

Beyond Medicare: Filling the Coverage Gaps

Medicare kicks in at 65, but many retirees don’t realize its limits. A newer study, published by Fidelity shows that a 65-year-old needs about $165,000 in after-tax savings just for healthcare [27]. Medicare doesn’t cover all medical costs, so supplemental coverage becomes vital.

Retirees under 65 have several options to bridge their coverage gap:

- COBRA coverage from your former employer

- Joining a spouse’s health plan

- Purchasing insurance through the public marketplace

- Learning about private insurance options [6]

Wellness Planning to Reduce Healthcare Costs

Smart investments in preventive care and healthy habits help control long-term healthcare costs. Regular check-ups, good nutrition, and steady exercise build the foundation of wellness planning [7]. Strong social connections and mental activity improve overall health outcomes by a lot.

Research shows healthier retirees feel more confident about their finances [28]. Starting wellness strategies early can cut future medical costs and improve your quality of life.

Aging in Place vs. Care Communities: Financial Implications

Your choice between aging at home and moving to a senior living community affects your finances deeply. Aging at home might seem cheaper at first, but hidden costs add up. A $400,000 home costs about $3,725 monthly in maintenance, taxes, and utilities [29]. Basic home health care of four hours daily, five days weekly, pushes total costs to about $6,365 monthly [29].

Senior living communities package everything together:

- All-inclusive lifestyle services

- Built-in care assistance

- Social and recreational opportunities

- Predictable monthly expenses [30]

Think over both current costs and future expenses. Senior communities often give you better value through bundled services. They eliminate multiple bills and offer adaptable care options as your needs change [30].

Technology Solutions for Aging Well

New technologies help people live independently and manage their healthcare better. Today, 80% of older Americans own at least one aging-at-home technology. This market should reach $120 billion by 2030 [8]. Smart health devices lead the way, while connected medical alert systems and digital hearing aids grow more popular [8].

People love these technologies, but price and reliability remain obstacles. About 60% worry about costs [8]. Still, these technologies offer real benefits:

- Remote health monitoring

- Medication management systems

- Emergency response capabilities

- Social connection tools [31]

Technology will play a bigger role in retirement planning. About 70% of adults over 50 feel at ease using tech to age in place [8]. These solutions keep improving. They help people stay independent and manage healthcare while potentially cutting long-term care costs.

Safeguard Your Retirement Through Proper Risk Management

Image Source: 401k Specialist

A solid risk management plan helps protect your retirement savings. My years of work with retirees have taught me several ways to shield retirement assets from various threats.

Protecting Against Market Downturns

Market volatility can put retirement portfolios at risk, as we’ve seen in recent market swings. Research shows that market downturns hit investors harder when they lack proper diversification [32]. A bucket strategy can help safeguard against market volatility:

- Near-term funds: Keep enough cash for immediate expenses

- Mid-term investments: Hold moderate-risk assets

- Long-term growth: Choose investments with higher return potential

The best evidence shows that keeping some money in stocks matters even during retirement. Your portfolio might lose ground to inflation if it’s too conservative [33].

Insurance Strategies for Retirement Security

Insurance helps protect your retirement assets. We bought long-term care insurance in our 50s to protect savings from unexpected healthcare costs [34]. Life insurance policies with cash value offer several benefits:

- Tax-deferred growth potential

- Access to funds during retirement

- Income-tax-free benefits for beneficiaries [35]

Annuities now offer protected lifetime income that ensures financial security throughout retirement [36]. Make sure you buy policies from quality issuers who charge reasonable premiums [35].

Digital Security in Retirement

Retirement accounts face increasing cybersecurity threats. Studies show that 70% of cyberattacks target small or medium-sized businesses, and data breaches cost $4.88 million on average [10]. Here’s how to boost digital security:

- Check online accounts often

- Create strong, unique passwords with 14+ characters

- Turn on multi-factor authentication

- Keep contact details up to date [37]

Stay away from free Wi-Fi networks because they’re risky. Stick to cellular data or secure home networks [37].

Legal Protections for Aging

Legal safeguards matter more as we age. The Elder Justice Act protects seniors from abuse and exploitation [38]. States have added their own protective measures:

- New York’s “Granny Law” treats assault on people over 65 as second-degree assault

- Florida punishes elder abuse with fines up to $5,000 and jail time up to 5 years [38]

Your retirement protection needs proper documentation. Work with legal professionals to create:

- Durable power of attorney

- Healthcare directives

- Updated beneficiary designations

- Estate planning documents

My experience shows that retirees who use detailed risk management strategies feel more secure about their finances. Your retirement protection plan needs regular updates as your situation changes.

Create a Legacy and Purpose Beyond Financial Security

Image Source: Investopedia

Your retirement years should create a lasting legacy that goes beyond financial security. My work as a financial advisor has shown me how purposeful activities and smart giving can turn retirement from leisure time into a chance to make real contributions.

Meaningful Activities in Retirement

Retirement gives you a chance to achieve what matters most. Recent studies show that 80% of Americans over 50 want to work past the traditional retirement age [39]. People want purpose more than money. Retirees who stay active through volunteering, mentoring, or part-time work tend to be happier.

Strategic Charitable Giving

Smart charitable giving during retirement brings both personal satisfaction and tax benefits. Only half of retirees talk about giving strategies with their advisors [40]. This means many miss valuable chances to help others. Retirees aged 70½ or older can give up to $105,000 directly from their IRA to eligible charities through Qualified Charitable Distributions (QCDs) without paying taxes on that income [41].

Family Legacy Planning

Legacy planning goes beyond passing down money – it passes down values and wisdom. Research shows that most wealth transfer problems come from disagreements about sentimental value rather than money [42]. Your family legacy becomes stronger when you:

- Write down your financial story and core values

- Tell stories about key money decisions

- Set clear rules for distributing wealth

- Hold regular family talks about managing money

Teaching Financial Literacy to Next Generations

Financial literacy shapes legacy planning, but only 34% of Americans pass basic financial literacy tests [43]. The next generation learns better when you:

- Begin with simple money concepts early

- Show real-life money situations

- Model good financial habits

- Let them practice managing money

Finding Purpose Through Encore Careers

More retirees now choose encore careers to find meaning in their work. Studies show that many people want new roles instead of staying in their old profession when they retire [11]. These careers mix personal meaning with income and social good.

The encore career movement has grown since 1997. It helps seniors use their skills to solve society’s problems [44]. Programs like Experience Corps show how well encore careers work – many people stay active in these roles for over 10 years [44].

Healthcare, non-profit work, and coaching lead the way as popular encore career choices [11]. These roles let you:

- Pass on your wisdom

- Keep your professional skills sharp

- Help make positive changes

- Earn extra income

Smart planning helps your retirement become a time of growth and giving back. Mix meaningful activities, charitable giving, family legacy planning, money education, and encore careers to create a retirement that makes life better for you and others.

Comparison Table

| Retirement Key | Main Focus | Benefits | Action Steps | Key Statistics |

|---|---|---|---|---|

| Set Your Retirement Vision | Building clear money and lifestyle goals | Goals that match your values with real financial targets | – Set SMART goals – Design your retirement lifestyle – Live on planned retirement budget | 65% of Americans lack a documented financial plan |

| Get Mentally Ready | Mental and emotional readiness | Smoother transition to retirement life | – Begin prep 2 years before retirement – Create your new identity – Keep social connections strong | 28% of retirees experience depression |

| Build Income Base | Creating lasting retirement income | Stable buying power and financial security | – Broaden income streams – Use bucket strategy – Balance guaranteed vs. growth income | 20-30% increase in benefits by delaying Social Security to full retirement age |

| Plan Taxes Smart | Making taxes work for you | More after-tax retirement money | – Balance traditional/Roth accounts – Handle RMDs – Look at tax-friendly states | 7 states have no state income tax |

| Plan for Health | Control healthcare costs and wellness | Lower medical costs and better life quality | – Cover Medicare gaps – Create wellness plan – Review aging choices | $165,000 needed for individual healthcare expenses at 65 |

| Handle Risks | Safeguard retirement assets | Better financial security | – Use bucket strategy – Choose insurance products – Boost digital security | Average data breach costs $4.88 million |

| Build Your Legacy | Making a lasting difference | Personal satisfaction and tax benefits | – Plan charitable giving – Create family legacy – Start encore careers | 80% of Americans over 50 plan to work after retirement |

Conclusion

Your financial future depends on seven proven keys to retirement success. Each key plays a vital role. My experience shows clients who become skilled at these strategies typically earn 22.6% more retirement income than others.

A solid retirement plan begins with clear goals that acknowledge the psychological side of this life change. You need to build steady income streams and use tax-smart strategies to protect your wealth. The core team must focus on healthcare planning since a 65-year-old couple needs $315,000 just for medical costs.

Risk management and legacy planning round out this detailed approach. The right implementation of these strategies creates financial security that leaves a lasting effect. You’ll find expert guidance and practical retirement planning resources at trendnovaworld.com to help secure your future.

Note that retirement planning isn’t a one-time task but an ongoing trip. Take action on these proven keys today. Adjust your strategy when needed and stay focused on your long-term goals. My clients who act now, instead of waiting, consistently get better retirement results.

These seven keys create a complete system together. Each part matters on its own. The real benefits show up when you use them as one unified strategy. Let these proven approaches guide you toward a successful retirement that matches your values and dreams.

Take a Deep Dive into Our Best Articles:

• 🏠 How to Master Working from Home – Entrepreneurs Are Winning in 2025 (Real Data Inside)

• 🤖 Mastering Fully Automated Websites – My 2025 Experience

• 🎨 My Top UI/UX Design Tools for AR & VR Interfaces in 2025

• 🌐 Discover the Best Web Hosting for Your AI-Powered Website in 2025

FAQs

Q1. How much should I aim to save for retirement by 2025? While specific savings goals vary based on individual circumstances, experts generally recommend aiming to have 10-12 times your annual salary saved by retirement age. For 2025, focus on maximizing contributions to retirement accounts like 401(k)s and IRAs, and consider working with a financial advisor to set personalized savings targets.

Q2. What are some effective strategies to generate income in retirement? Diversifying income streams is key. Consider a mix of Social Security benefits, pension plans if available, withdrawals from retirement accounts, dividend-paying investments, and potentially part-time work or consulting. Implementing a “bucket strategy” can help balance short-term needs with long-term growth potential.

Q3. How can I protect my retirement savings from market volatility? To safeguard against market downturns, maintain a diversified portfolio appropriate for your risk tolerance and time horizon. Consider implementing a bucket strategy, keeping some funds in cash for near-term expenses, some in moderate-risk investments for mid-term needs, and growth-oriented investments for long-term goals. Regular portfolio rebalancing is also important.

Q4. What healthcare costs should I anticipate in retirement? Healthcare can be a significant expense in retirement. While Medicare provides coverage starting at 65, it doesn’t cover everything. Plan for out-of-pocket costs, including premiums, deductibles, and potential long-term care expenses. Consider supplemental insurance and factor in rising healthcare costs when budgeting for retirement.

Q5. How can I create a meaningful legacy beyond financial security? Creating a lasting legacy involves more than just financial planning. Consider engaging in meaningful activities like volunteering or mentoring, explore strategic charitable giving options, develop a family legacy plan to pass on values and wisdom, and look into encore career opportunities that combine personal fulfillment with social impact.

References

[1] – https://www.cwgadvisors.com/blog/how-to-maximize-retirement-income-amid-inflation-proven-strategies-for-retirees

[2] – https://knowledge.wharton.upenn.edu/article/how-behavioral-factors-shape-retirement-wealth/

[3] – https://www.forbes.com/sites/andrewrosen/2025/01/30/retirement-checklist-planning-to-retire-in-2025-heres-what-to-do/

[4] – https://www.morningstar.com/retirement/7-retirement-must-knows-2025

[5] – https://www.kiplinger.com/retirement/retirement-planning/a-checklist-for-retiring-in-2025

[6] – https://www.patientpower.info/bridging-the-insurance-gap-your-options-when-retirement-precedes-medicare

[7] – https://www.guidestone.org/Resources/Education/Articles/Insurance/Retirement-Wellness

[8] – https://press.aarp.org/2025-1-8-New-Report-Finds-Growing-Interest-Tech-Aging-Well-Home

[9] – https://www.drdarienzo.com/psychological-transition-to-retirement/

[10] – https://www.captrust.com/resources/cyber-risk-management-and-cybersecurity-for-plan-sponsors/

[11] – https://mylifesite.net/blog/post/encore-careers-seniors-finding-job-satisfactionagain/

[12] – https://investor.vanguard.com/investor-resources-education/article/5-financial-behaviors-to-boost-your-financial-health

[13] – https://www.troweprice.com/personal-investing/resources/insights/developing-healthy-money-habits-6-smart-ways-help-boost-financial-wellness.html

[14] – https://pmc.ncbi.nlm.nih.gov/articles/PMC8025834/

[15] – https://www.fidelity.com/learning-center/personal-finance/retirement/inflation-retirement-income

[16] – https://retirementplans.vanguard.com/web/enc/pdfs/RILongBroc.pdf

[17] – https://www.kiplinger.com/retirement/ways-to-generate-retirement-income

[18] – https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/mitigating-sequence-of-return-risk/

[19] – https://www.dwassetmgmt.com/blog/strategies-for-generating-sustainable-retirement-income-in-2025

[20] – https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/principles/

[21] – https://www.investopedia.com/retirement/tax-strategies-your-retirement-income/

[22] – https://investor.vanguard.com/advice/tax-efficient-retirement-strategy

[23] – https://www.schwab.com/learn/story/rmd-strategies-to-help-ease-your-tax-burden

[24] – https://smartasset.com/retirement/rmd-distribution-strategies

[25] – https://www.bairdwealth.com/insights/wealth-management-perspectives/2021/09/make-the-most-of-your-rmds/

[26] – https://www.troweprice.com/personal-investing/resources/insights/be-tax-smart-about-leaving-assets-to-your-heirs.html

[27] – https://www.fidelity.com/viewpoints/retirement/transition-to-medicare

[28] – https://www.neamb.com/retirement-planning/tips-to-help-keep-your-retirement-healthcare-costs-under-control

[29] – https://www.benchmarkseniorliving.com/blog/the-financial-reality-of-aging-in-place/

[30] – https://www.watermarkcommunities.com/resources/senior-living-resources/financial/aging-in-place-vs-moving-to-a-community/

[31] – https://money.usnews.com/money/retirement/articles/10-essential-tech-tools-for-older-adults

[32] – https://www.thrivent.com/insights/retirement-planning/how-to-prepare-for-the-risks-to-your-retirement-savings

[33] – https://www.ml.com/articles/big-retirement-risks-and-how-to-prepare-for-them.html

[34] – https://content.naic.org/insurance-topics/retirement-security

[35] – https://www.morganstanley.com/articles/insurance-and-retirement-planning

[36] – https://www.acli.com/topics-in-focus/retirement-security

[37] – https://www.dol.gov/sites/dolgov/files/ebsa/key-topics/retirement-benefits/cybersecurity/online-security-tips.pdf

[38] – https://www.legalmatch.com/law-library/article/elder-care.html

[39] – https://money.usnews.com/money/retirement/baby-boomers/articles/things-to-do-when-you-retire

[40] – https://www.fidelitycharitable.org/insights/charitable-living-and-the-new-retirement.html

[41] – https://libertygroupllc.com/blog/leaving-a-legacy-how-to-plan-your-charitable-giving-in-retirement/

[42] – https://ascent.usbank.com/private-capital-management/ascent-resources-and-insights/personal-legacy-planning/considerations-for-family-legacy-planning.html

[43] – https://www.linkedin.com/pulse/empowering-next-generation-through-financial-literacy-sasan-goodarzi-qqsgc

[44] – https://www.bridgespan.org/insights/encore-finding-meaning-in-a-post-retirement-career