These 12 retirement planning strategies come directly from successful retirees’ playbooks. The practical methods line up with the time-tested 4% withdrawal rule and the principle of saving 25 times your living expenses.

Nearly 70% of people aged 65 or older will need some form of long-term care. This reality makes retirement planning more significant now, especially since Medicare costs will triple from $500 to $1,500 monthly by age 95.

People recognize retirement strategies’ importance but rarely understand their full impact. The math tells an compelling story – a monthly $50 investment at 7% return builds to more than $130,000 over 40 years. My experience as a financial expert shows wealthy retirees create their comfortable retirement through deliberate, proven approaches.

These 12 retirement planning strategies come directly from successful retirees’ playbooks. The practical methods line up with the time-tested 4% withdrawal rule and the principle of saving 25 times your living expenses. Let me show you how to implement these secrets and secure your financial future.

They Distinguish Between Money and True Wealth

Image Source: Acorns

“Financial freedom is a mental, emotional, and educational process.” — Robert Kiyosaki, Founder of Rich Dad Company, bestselling author of Rich Dad Poor Dad

Successful retirees know that real wealth means more than just money in the bank. Recent studies show that while 74% of preretirees focus on financial planning, only 35% get ready emotionally for retirement [1]. These numbers show why wealthy retirees take a different path to retirement planning.

Understanding Financial Independence vs. Material Possessions

Financial independence lets you work because you want to, not because you must. It gives you the freedom to choose when you work, what work you do, and how much you work [2]. Research reveals that 57% of retired adults never thought about planning their emotional health in retirement [3]. This shows how people often put material wealth ahead of their overall well-being.

How Wealthy Retirees Define Success

Smart retirees know retirement isn’t about spending their savings. They balance between using their money and making it last their lifetime [4]. About 49% of retirees say they spend carefully or very carefully [3]. This shows they understand that success isn’t about expensive living.

Building Wealth Beyond the Bank Account

Wealthy retirees focus on several key areas:

- Physical and mental health

- Strong relationships and social bonds

- Ways to keep learning and growing

- Making a difference in their community

Research proves that loneliness and lack of friends directly affect older adults’ physical and mental health [3]. Smart retirees put their money into experiences that make them happy instead of buying more things.

The Mindset Shift That Creates Lasting Security

New retirees often struggle to switch from saving money to spending it wisely [5]. Successful retirees welcome this change. They focus on making the most of their time and energy rather than living extravagantly. Retirement should match what matters most to them [6].

These retirees keep large emergency funds and create several income sources to stay secure. They also know that staying healthy might be their most important investment [5]. This complete approach gives them both financial security and personal satisfaction throughout retirement.

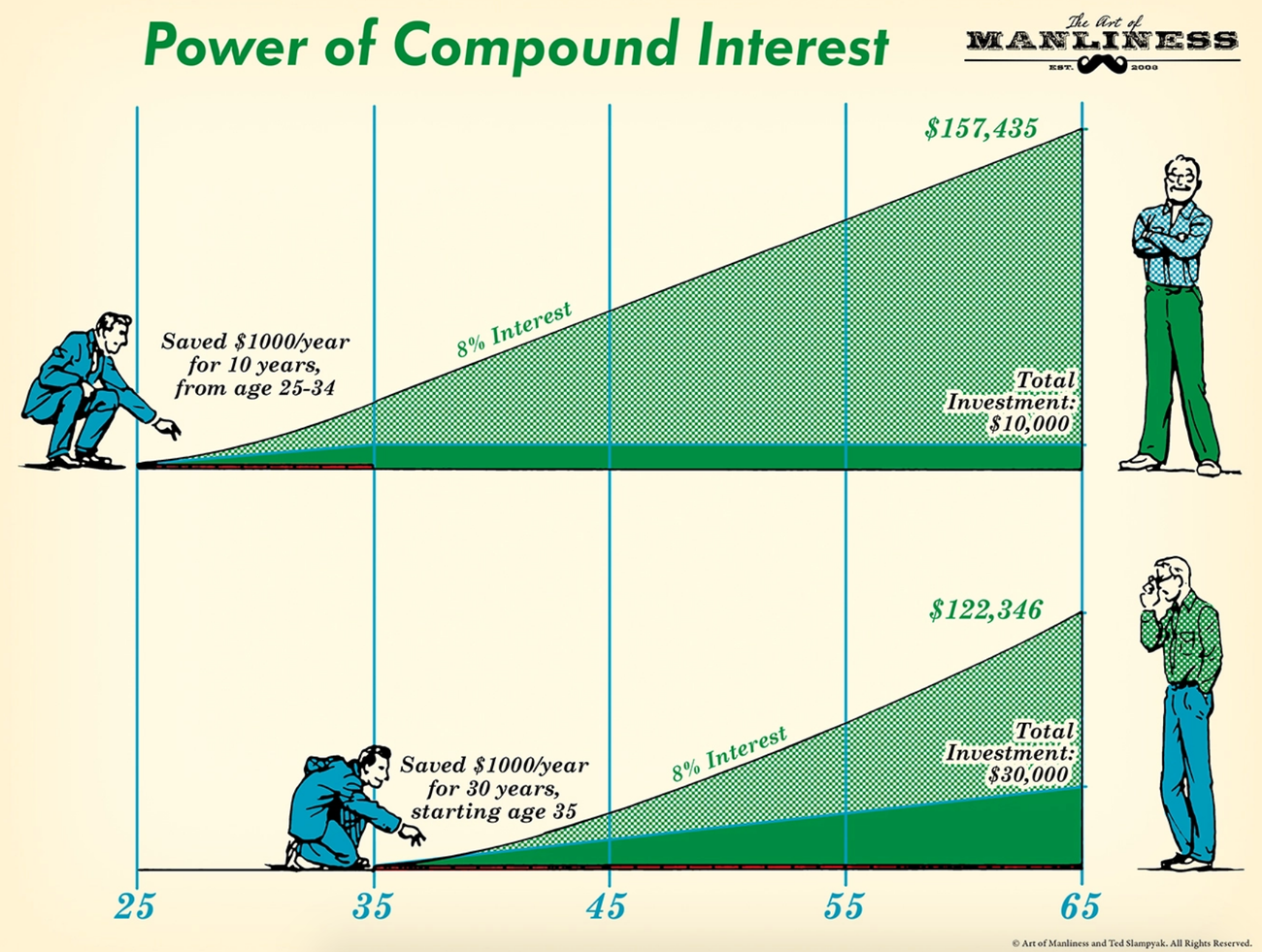

They Start Early and Leverage Compound Growth

Image Source: Bautis Financial

Time proves to be your greatest ally when planning for retirement. My experience as a financial advisor shows early investors consistently outperform those who start late, even with smaller contributions.

The Mathematical Magic of Starting in Your 30s

Let’s look at this powerful example: A 30-year-old professional earning $80,000 annually who invests 10% of their salary through a 401(k) can accumulate approximately $1.5 million by age 65 [7]. A $1,000 investment with a 5% yearly interest rate yields $276 over five years. The same amount invested annually for 50 years could build savings of $220,000 [8].

How Small, Consistent Investments Grow Exponentially

Compound interest turns modest investments into substantial wealth. A $2,000 investment earning 8% interest annually grows to $2,160 in the first year. The following year produces $172.80 on the increased balance, creating a new total of $2,332.80 [8].

Real-life results show this stark contrast between early and delayed investing:

- An early investor contributing $70,000 over their first decade ended up with $2,345,689

- A late starter investing $217,000 over the subsequent years achieved only $1,483,432 [8]

Mathematics favors those who start early. A minimal weekly investment of $12 at age 35 could grow to $110,000 by age 67 [7].

Recovery Strategies for Late Starters

Late starters can accelerate their retirement savings through these proven strategies:

- Maximize catch-up contributions after age 50 [9]

- Launch a side business for additional income streams

- Review downsizing options to redirect funds toward retirement

- Create a detailed budget to identify potential areas for increased savings

Late starters should focus on aggressive saving while maintaining a strategic investment approach. A qualified financial advisor becomes especially valuable as they help answer three fundamental questions [9]:

- Required capital needs

- Regular savings needed

- Optimal investment strategies for success

Compound growth remains one of the simplest yet powerful tools to build retirement wealth [10]. Small, regular contributions create meaningful results over time, especially when combined with tax-advantaged retirement accounts and employer matching programs.

They Diversify Investments Strategically

Image Source: Sophisticated Investor

Diversification is the life-blood of successful retirement planning. Research shows a well-diversified portfolio helps manage risk at any level an investor targets [11].

Beyond the Simple Stock-Bond Mix

Smart retirees know true diversification goes beyond holding stocks and bonds. A reliable portfolio has investments in sectors, market capitalizations, and investment styles of all types [12]. Ultra-high-net-worth investors now allocate 50% of their assets to alternative investments, while average investors allocate just 5% [13].

Alternative Investment Vehicles Wealthy Retirees Favor

Wealthy retirees add several alternative investments to their strategy:

- High-net-worth family office portfolios’ private equity makes up 27% [13]

- Infrastructure projects that generate steady income through user fees

- Private market investments that have shown consistent returns from 2016 through 2023 [14]

Geographic Diversification Strategies

International diversification protects against country-specific risks. Successful retirees spread their investments across different regions because various markets often perform differently during economic cycles [15]. Their strategy includes both developed and emerging markets to capture growth opportunities worldwide [12].

Real Estate’s Role in Retirement Portfolios

Real estate is a vital component in retirement portfolios and offers dual benefits of potential appreciation and income generation. Wealthy retirees approach real estate investment through:

- Direct property ownership for rental income

- Real Estate Investment Trusts (REITs) for passive participation

- Real estate crowdfunding platforms for diversified exposure [16]

Real estate investments appreciate over time and offer protection against inflation as demand associates positively with GDP growth [17].

Portfolio Rebalancing Frequency

The right asset mix needs regular attention. Research shows annual rebalancing works best for most investors [18]. This approach lets investors:

- Harvest the equity risk premium effectively

- Generate lower transaction costs compared to frequent rebalancing

- Keep risk levels consistent with long-term goals [18]

Successful retirees rebalance when an asset class shifts 5-10% from its target allocation [12]. They avoid excessive rebalancing during market volatility because transaction costs rise in turbulent periods [18].

A diversified approach proves its value consistently and helps manage sequence-of-returns risk without sacrificing growth potential. Wealthy retirees create resilient portfolios by spreading investments across multiple asset classes, sectors, and geographies that weather various market conditions [11].

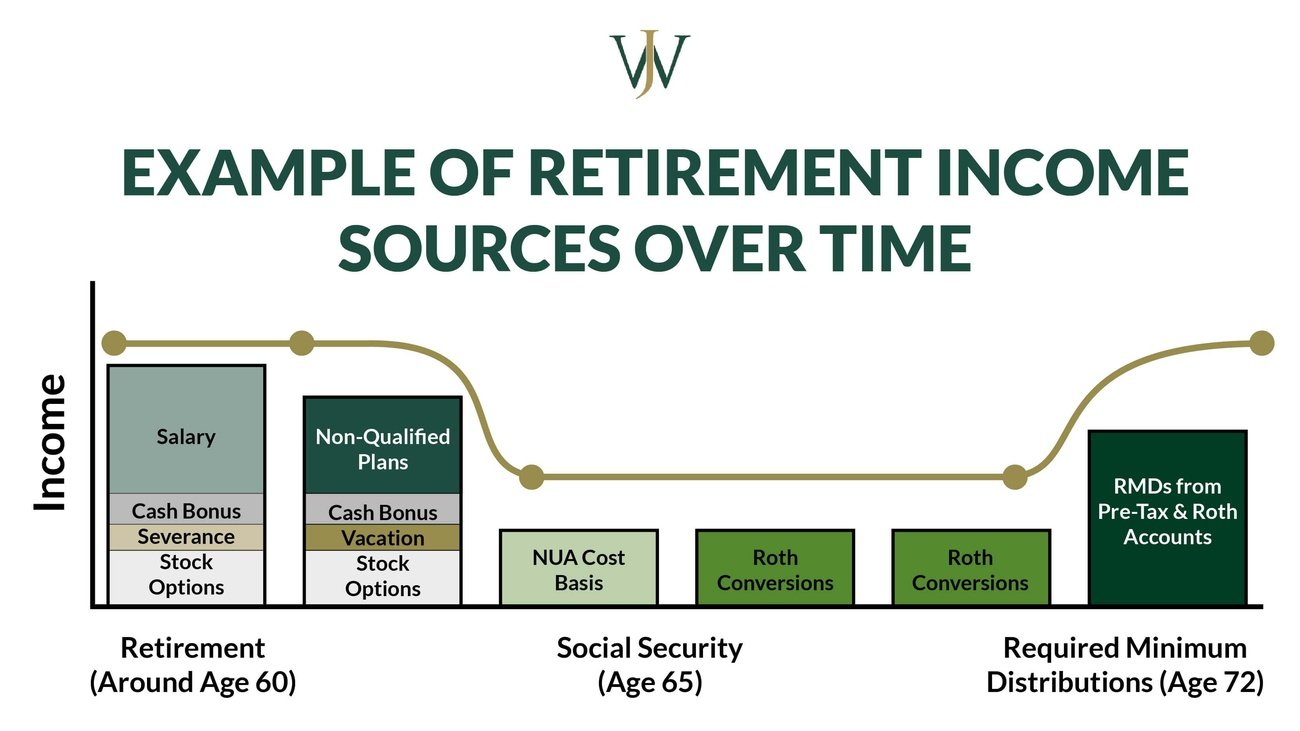

They Optimize Tax Planning Years Before Retirement

Image Source: Willis Johnson & Associates

Tax planning is a vital element to build retirement wealth. My analysis of tax-optimization strategies reveals several approaches that give better results.

Strategic Roth Conversion Ladders

A Roth conversion ladder gives you a quick way to access retirement funds before age 59½ without incurring penalties [19]. This strategy converts traditional retirement account funds to a Roth IRA in smaller increments over multiple years. Starting five years before you need the money will give you penalty-free withdrawals [20]. Market downturns are the best time to execute these conversions to maximize tax benefits [2].

Tax-Loss Harvesting Techniques

Tax-loss harvesting turns investment losses into valuable tax savings. Selling securities at a loss lets investors offset capital gains and reduce ordinary income by up to $3,000 annually [6]. Tax savings reinvested in the portfolio make up 37% of tax-loss harvesting success [6]. Investors must handle the wash-sale rule carefully. This rule stops you from claiming losses if you buy similar securities within 30 days [21].

Geographic Tax Arbitrage

Moving to low-tax regions is a smart way to boost retirement savings. States without income tax like Florida or Texas can reduce your tax burden [22]. Research is vital since some tax-free states have higher property taxes [22]. Remote work has made this strategy more available. You can earn in high-income areas while living in low-cost regions [22].

Charitable Giving as a Tax Strategy

Well-structured charitable contributions offer multiple tax advantages. Qualified Charitable Distributions (QCDs) let people aged 70½ or older donate up to $100,000 yearly directly from their IRAs. This reduces taxable income [23]. Donor-advised funds give immediate tax deductions and let you distribute charitable grants strategically over time [24].

Key charitable giving strategies include:

- Donating appreciated assets to avoid capital gains tax

- Combining multiple years’ deductions into one year

- Using charitable remainder trusts for tax-efficient estate planning

Smart implementation of these tax optimization techniques creates significant long-term savings. Early planning and consistent execution are essential to maximize these benefits throughout retirement.

They Assemble a Team of Trusted Financial Professionals

Image Source: Charles Schwab

The difference between average and wealthy retirees often comes down to having a reliable team of financial professionals. A skilled financial team helps you prepare for retirement and avoid mistakes that can get pricey and derail your retirement goals [3].

When to Hire a Fiduciary Financial Advisor

Fiduciary advisors have a legal and ethical duty to put their client’s interests first [4]. You should work with a fiduciary advisor when you start your career or go through major life changes. Fee-only advisors charge either an hourly rate, flat annual fee, or about 1% of managed assets [25].

The Role of Estate Planning Attorneys

Estate planning attorneys help organize your assets so they transfer smoothly after death [26]. They use tools like durable powers of attorney and healthcare directives to make sure your retirement funds match your wishes, even if you become incapacitated [27].

Tax Professionals Who Specialize in Retirement

Tax specialists are a great way to get solid distribution strategies for your retirement. You should partner with a tax professional if you:

- Have several retirement investments with different tax implications

- Need to plan tax deductions strategically

- Want to minimize your lifetime tax burden

- Have large tax-deferred accounts [28]

How to Evaluate Financial Advice

Here’s how to assess potential financial advisors:

- Check their credentials and education

- Get referrals from people you trust

- Ask about their research methods for products they recommend

- Learn how they get paid [3]

Finding the right team takes a full picture of each professional. Ask advisors about their business approach and if they earn commissions from their recommendations [29]. Trustworthy professionals will openly share this information so you can decide about possible conflicts of interest.

The best retirement planning comes from professionals with specialized credentials like Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), or Retirement Income Certified Professional (RICP) [30]. These credentials show their expertise in retirement planning and managing investments.

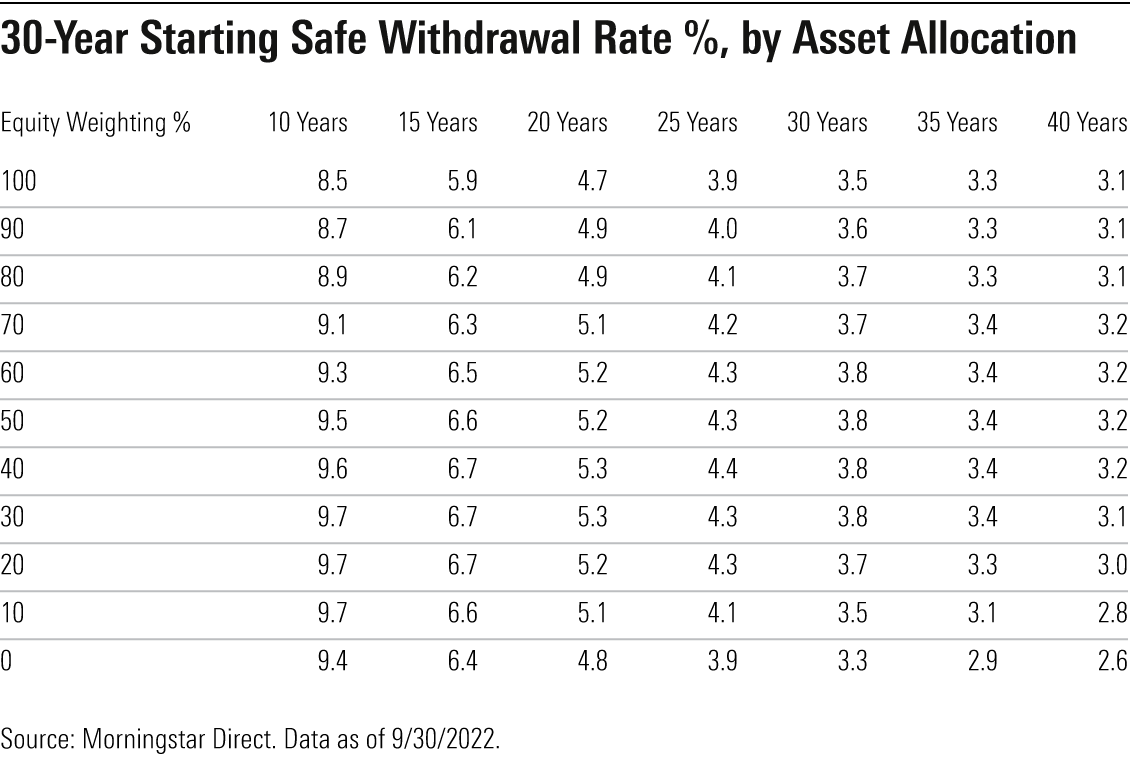

They Determine and Stick to Safe Withdrawal Rates

Image Source: Morningstar

“Retirement is like a long vacation in Las Vegas. The goal is to enjoy it the fullest, but not so fully that you run out of money.” — Jonathan Clements, Former personal finance columnist for The Wall Street Journal

Retirement planning today just needs a smart way to handle withdrawal rates. Recent research from Morningstar suggests adjusting the traditional 4% rule to 3.7% for 2025. This adjustment gives retirees a 90% chance their funds will last through retirement [1].

Beyond the 4% Rule: Modern Withdrawal Strategies

The traditional 4% rule often leaves retirees with excess money at death. Many end up with six times their starting amount after 30 years [31]. Smart retirees now adopt alternative strategies like spending guardrails that set withdrawal limits between 4% and 6% [31].

Dynamic Spending Adjustments During Market Volatility

Dynamic spending proves a powerful strategy that lets retirees:

- Cut back withdrawals in down markets

- Spend more during market upswings

- Keep their portfolio healthy through market cycles

Research shows that skipping inflation adjustments after market declines works better than temporary spending cuts [32]. Small permanent adjustments also protect retirement assets better than large temporary cuts [32].

Creating Multiple Income Streams for Stability

Successful retirees arrange their basic expenses with guaranteed income sources. A smart plan includes:

- Waiting to claim Social Security benefits until age 70

- Building bond ladders to get steady income

- Using Required Minimum Distributions (RMDs) as a baseline for withdrawals

Yale’s endowment model offers a different point of view. It suggests a mixed approach – 70% from last year’s distributions with inflation adjustment plus 30% based on the portfolio’s three-year average balance [31].

Smart retirees know that one withdrawal strategy can’t fit everyone’s needs. They think over market conditions, personal needs, and risk tolerance to develop flexible approaches. This balances their current lifestyle with long-term security. Setting guardrails and adjusting based on market performance helps these retirees stay financially stable throughout retirement [33].

They Prioritize Health as a Financial Asset

Image Source: Finance Strategists

Health investments matter just as much as financial planning when it comes to retirement success. Workers who score better on financial well-being tests show better mental health outcomes consistently [34].

The ROI of Preventative Healthcare

Smart investments in preventative care deliver remarkable returns. Studies show that spending just $10 per person each year on community-based prevention programs saves $16 billion nationwide within five years [35]. Public health programs give back $14.30 for every dollar invested, which makes an even stronger case [36].

Long-term Care Insurance Strategies

Starting your long-term care planning early makes sense – ideally in your 50s or sooner [37]. Assisted living now costs $6,650 monthly, while nursing home care runs $11,756 [37]. Smart retirees look at hybrid policies that combine long-term care coverage with death benefits. These policies protect against premium increases that hit 70-80% of traditional policy holders [5].

Mental Health Investments That Pay Dividends

Your mental wellness directly affects your financial security. People with psychological distress keep retirement savings 67% lower than those without such issues [34]. New legislation now extends Medicare coverage to include behavioral health services, marriage counseling and mental health support [38].

How Medical Tourism Fits Into Their Planning

Medical tourism has become a viable way to manage healthcare costs. Procedures in other countries often cost just one-third to one-tenth of U.S. prices [39]. Thailand, Colombia, and Malta provide world-class healthcare with highly trained medical teams and modern equipment [39].

Successful retirees know good health means more than regular exercise. They build complete strategies that cover preventative care, mental wellness, and innovative healthcare access. Many save substantially on healthcare costs through employer-based health programs within 2-3 years [40]. This integrated approach to health as a financial asset helps maintain both physical and financial stability throughout retirement.

They Manage Debt Strategically

Image Source: Covenant Wealth Advisors

Debt management is a powerful tool in retirement planning. Recent studies show that high-net-worth individuals use debt differently. They see certain types of loans as ways to build wealth [7].

Good Debt vs. Bad Debt in Retirement

The right classification of debt plays a vital role in retirement success. Good debt usually has interest rates below 6% and helps boost net worth or create future income [41]. Bad debt includes high-interest obligations like credit cards, where average balances reach $6,500 [41]. Smart retirees know mortgages can be beneficial debt. Homes are the biggest asset for most Americans, with median equity values of $299,000 [41].

Using Low-Interest Debt to Grow Investments

Wealthy retirees use debt wisely to boost investment returns. They borrow at lower rates to invest in higher-yielding opportunities, which can improve their returns [42]. Margin loans against investment portfolios are a quick way to access capital without formal credit applications [42]. Home equity lines of credit also give flexible borrowing options at good rates [43].

Mortgage Strategies for Wealthy Retirees

Smart retirees put sophisticated mortgage approaches to work. Home equity averages $174,000 while retirement accounts typically hold $76,000 [7]. Wealthy retirees use several strategies to bridge this gap:

- They refinance existing mortgages into reverse mortgages to eliminate monthly payments

- They use HECM for Purchase programs to downsize efficiently

- They keep mortgages for tax advantages [7]

Housing costs make up 35% of retirement expenses, about $18,000 each year [7]. Smart debt management helps successful retirees turn their biggest expense into a wealth-building tool. They also use reverse mortgage lines of credit as flexible funding sources that provide emergency reserves without touching investment accounts [7].

Prosperous retirees know debt management means finding the right balance between opportunities and risks. They keep substantial cash reserves alongside their borrowed positions to create strong financial structures that preserve wealth long-term [43].

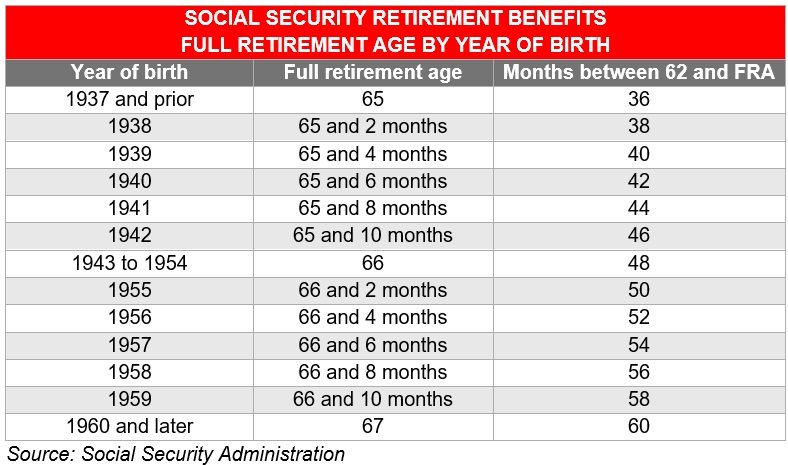

They Optimize Social Security Benefits

Image Source: Investment News

Social Security benefits serve as the life-blood of retirement income. These steady, inflation-protected payments throughout retirement make smart planning and decision-making vital for long-term financial security.

Timing Strategies That Maximize Lifetime Benefits

The rewards of delaying Social Security claims can be substantial. Your benefits increase by 8% for each year you wait beyond full retirement age [8]. Monthly payments could reach $5,108 in 2025 for people who paid maximum taxes during their careers [8]. Your future payments might even go up if you keep working after claiming benefits since your earnings continue to count toward your record [8].

Spousal Benefit Coordination Techniques

Married couples have special advantages when planning Social Security. You can claim benefits based on your own work history or receive up to 50% of your partner’s benefit at full retirement age [10]. Couples with big differences in their earnings might find spousal benefits more valuable [44].

Here’s what you need to know:

- Monthly reductions in spousal benefits reach 25/36 of one percent before normal retirement age [10]

- Benefits drop another 5/12 of one percent for each month beyond 36 months [10]

- Spouses must be 62 or older, or have eligible children in their care to qualify [10]

Tax-Efficient Social Security Planning

Your Social Security benefits improve with smart tax planning. The government calculates your combined income by adding your adjusted gross income, nontaxable interest, and half of your Social Security benefits [45]. Single filers with combined income under $25,000 ($32,000 for joint filers) won’t pay federal taxes on their benefits in 2025 [45].

Social Security benefits face state taxes in all but one of these states: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, Vermont, and West Virginia [45]. You can reduce your overall tax burden through careful planning of withdrawals and management of other income sources.

Smart choices about timing, spousal benefits, and tax implications help create stronger retirement income streams. These decisions shape your lifetime Social Security benefits and financial security during retirement.

They Maintain Substantial Emergency Reserves

Image Source: Bankrate

Smart emergency fund management sets wealthy retirees apart from others. Studies show about 84% of retirees between 60-78 years keep dedicated emergency savings [46]. This highlights how crucial emergency funds are in retirement planning.

Beyond the Standard 3-6 Months

The usual emergency fund advice doesn’t work well for retirees. Financial experts support keeping 12-18 months of living expenses [47]. We mainly see this because of higher healthcare costs and fewer ways to generate income. Retirees who depend heavily on investment income should keep 24 months of expenses ready [47].

Strategic Cash Management in Retirement

Wealthy retirees use smart cash management strategies:

- They add 1-2% of their home’s value yearly for possible repairs [47]

- Their emergency funds grow by 2-3% each year to fight inflation [47]

- They set aside an extra 10-15% for travel emergencies [47]

How They Protect Against Sequence of Returns Risk

Sequence risk creates unique challenges early in retirement. A large emergency fund helps avoid selling assets when markets drop [48]. Successful retirees use bucket strategies to manage their money:

- Short-term bucket: Three years of living expenses in cash equivalents

- Intermediate bucket: Low-risk investments they can tap into

- Long-term bucket: Growth investments to protect against inflation [9]

Using Lines of Credit as Emergency Backups

Smart retirees set up Home Equity Lines of Credit (HELOCs) before they stop working [49]. These credit lines work as backup emergency funds and offer key benefits:

- They can access substantial funds without selling investments

- Interest rates stay lower than traditional loans

- They have flexibility when unexpected costs come up [49]

Getting credit lines before retirement makes sense because qualifying becomes harder after retirement [50]. Wealthy retirees keep funds easily available through high-yield savings accounts or short-term CD ladders [47] among other backup options. They regularly check if their emergency reserves meet their needs throughout retirement as expenses, health, and market conditions change [47].

They Live With Purpose Beyond Finances

Image Source: Investopedia

A strong sense of purpose stands out as a key factor in retirement success that goes way beyond the reach and influence of financial security. Studies show that people who have a clear purpose in life cut their mortality risk by 15.2% compared to those who don’t [51].

How Wealthy Retirees Find Fulfillment

Well-off retirees find purpose through several paths:

- Family and relationships

- Community involvement

- Learning new skills

- Taking part in meaningful hobbies [51]

These activities boost emotional well-being among other benefits like financial stability. The numbers tell an interesting story – 97% of retirees who keep a reliable sense of purpose say they’re happy, while only 76% of those without direction feel the same [11].

The Connection Between Purpose and Longevity

Science backs up how purposeful living affects how long we live. A detailed study with 7,000 adults over 50 showed lower death rates in people who scored highest on life purpose scales [51]. This connection works in three main ways:

- Better health protection through improved sleep, nutrition, and preventive care

- Better handling of stress and quicker bounce-back from tough times

- Less inflammation connected to heart conditions [51]

The numbers are striking – women with strong purpose lower their chance of early death by 34%, while men see a 20% drop [52].

Balancing Leisure and Contribution

Smart retirees know their free-time activities should line up with their core values. They make a real difference through volunteering, helping their community, or mentoring others while enjoying their retirement freedom [53]. Research keeps showing that staying socially active is crucial for brain health and emotional happiness [53].

People who retire with purpose often choose semi-retirement. This gives them time to enjoy life and give back [54]. Such a balanced approach helps prevent retirement anxiety, which troubles more than half of adults over 40 [11]. By seeing success as more than just money in the bank, these retirees build a life filled with both joy and meaning.

Smart planning and thoughtful involvement show how purpose-driven retirement leads to personal satisfaction and better health. Their approach proves that true success in retirement covers more than just having enough money – it’s about making the most of life’s opportunities [11].

They Plan for Cognitive Decline and Estate Transfer

Image Source: Legacy Assurance Plan

Protecting assets from cognitive decline needs careful planning. Financial crimes against the elderly often involve misuse of funds, property, and assets. These crimes also include fraud and identity theft [55].

Legal Protections Against Financial Exploitation

The year 2023 saw 34 states take action against financial exploitation of elderly adults [55]. Florida set specific conditions that define exploitation of people aged 65 or older. The state outlined first, second, and third-degree felonies [55]. Georgia created new procedures that let broker-dealers report suspected exploitation [55]. These rules now allow temporary holds on disbursements to protect seniors from financial abuse.

Digital Asset Management Strategies

Digital estate planning has become vital as our online presence grows. A complete digital inventory has:

- Social media and email accounts

- Online banking and investment platforms

- Cryptocurrency keys and digital collections

- Cloud storage with photos and documents [14]

Smart retirees use password management software like LastPass or 1Password. These tools need just one master password for executor access [14]. They also pick digital executors to handle their online assets [13].

Family Communication Protocols

Good communication helps prevent future conflicts. Wealthy retirees set up family meetings to talk about estate plans. They think over:

- Who should attend (immediate family vs. in-laws)

- What information to share

- When to have these talks [56]

These meetings work best with proper planning, clear agendas, and professional help if needed [56].

Legacy Planning Beyond Money

A true legacy goes beyond financial assets. It includes values, experiences, and life lessons. Successful retirees share their experiences through written stories, audio recordings, or video messages [57]. Many create scholarship funds or help charitable causes that match their values [57].

Ethical wills help pass down philosophical insights and moral teachings [58]. Some retirees write letters to their grandchildren and share wisdom about resilience, empathy, and curiosity [58]. This approach gives both financial security and leaves a lasting effect across generations.

Comparison Table

| Strategy | Key Principle | Implementation Timeline | Main Benefits | Notable Statistics |

|---|---|---|---|---|

| Distinguish Between Money and True Wealth | Focus on integrated well-being beyond financial metrics | Pre-retirement | Balanced approach between decumulation and preservation | 74% focus on financial planning, but only 35% prepare emotionally |

| Start Early and Make Use of Compound Growth | Time is the most powerful investment ally | 30s or earlier | Exponential growth of investments | $80,000 salary invested at 10% can reach $1.5M by age 65 |

| Vary Investments Strategically | Spread investments in multiple asset classes | Throughout retirement planning | Risk management and better returns | 50% of ultra-high-net-worth portfolios in alternative investments |

| Optimize Tax Planning | Tax reduction through multiple approaches | 5+ years before retirement | Lower tax burden and increased wealth preservation | Up to $3,000 annual tax savings through loss harvesting |

| Build Professional Team | Create network of specialized advisors | Early career or major life changes | Complete expertise and risk mitigation | ~1% of managed assets for fee-only advisors |

| Determine Safe Withdrawal Rates | Calculate sustainable spending levels | Pre-retirement | Portfolio longevity and stable income | 3.7% recommended withdrawal rate for 2025 |

| Treat Health as Financial Asset | Invest in preventative care and wellness | Throughout life | Lower healthcare costs and increased longevity | $10 per person in prevention yields $16B in savings |

| Handle Debt Strategically | Use good debt while eliminating bad debt | Pre-retirement | Better wealth building opportunities | Average home equity of $299,000 |

| Optimize Social Security Benefits | Maximize lifetime benefits through timing | Age 62-70 | Higher guaranteed lifetime income | 8% annual increase in benefits for delayed claiming |

| Keep Emergency Reserves | Maintain substantial liquid assets | Throughout retirement | Protection against market volatility | 12-18 months of expenses recommended |

| Find Purpose Beyond Finances | Focus on meaningful activities and relationships | Throughout retirement | Better longevity and satisfaction | 15.2% reduced mortality risk with strong purpose |

| Prepare for Cognitive Decline | Set up legal and financial safeguards | Pre-retirement | Asset protection and smooth wealth transfer | 34 states addressed elderly financial exploitation in 2023 |

Key Takeaways

You just need more than simple financial knowledge to plan your retirement well. I’ve spent years advising clients and seen how these 12 strategies help create lasting wealth and security for retirees.

Smart retirees know that true wealth goes beyond money. They make an early start, broaden their investments wisely, and optimize taxes while keeping substantial emergency reserves. Their success comes from working with qualified professionals who help determine safe withdrawal rates and manage debt effectively.

Your health is a crucial investment, since 70% of retirees will need long-term care. Successful retirees also get the most from Social Security benefits through careful timing and coordination with their spouses. They find purpose beyond finances, which reduces mortality risk by 15.2%.

New research suggests we should adjust traditional withdrawal rates to 3.7% for 2025. This shows how retirement strategies must adapt to changing economic conditions. You can find the latest retirement planning insights and strategies at trendnovaworld.com, where we share expert financial guidance regularly.

A successful retirement comes from careful planning that covers your financial, physical, and emotional well-being. Start using these proven strategies today to build your path toward a secure retirement you’ll enjoy.

Maximize Your Knowledge – Read More Below:

• 🏠 How to Master Working from Home – Entrepreneurs Are Winning in 2025 (Real Data Inside)

• 🤖 Mastering Fully Automated Websites – My 2025 Experience

• 🎨 My Top UI/UX Design Tools for AR & VR Interfaces in 2025

• 🌐 Discover the Best Web Hosting for Your AI-Powered Website in 2025

FAQs

Q1. How much should I save to generate $100,000 annual retirement income? To generate $100,000 yearly income in retirement, you’d need approximately $2.5 million saved, based on the 4% withdrawal rule. However, this amount can vary depending on factors like your lifestyle, investment strategy, inflation, healthcare costs, and location.

Q2. What is the 7% rule for retirement planning? The 7% rule suggests withdrawing 7% of your total retirement savings in the first year and adjusting that amount for inflation in subsequent years. While this can help maintain financial stability, it’s not considered a safe withdrawal rate and assumes your remaining investments will continue to grow.

Q3. How can I optimize my Social Security benefits? To maximize Social Security benefits, consider delaying your claim until age 70, as this increases your benefit by 8% annually beyond full retirement age. For married couples, coordinate spousal benefits and evaluate strategies like “file and suspend” to potentially increase lifetime payouts.

Q4. Why is maintaining an emergency fund important in retirement? An emergency fund in retirement protects against unexpected expenses and market volatility. Financial experts recommend keeping 12-18 months of living expenses in easily accessible accounts, which helps avoid forced asset sales during market downturns and provides peace of mind.

Q5. How can I plan for potential cognitive decline in retirement? To safeguard against cognitive decline, establish legal protections like power of attorney and healthcare directives. Create a comprehensive digital asset inventory, implement family communication protocols, and consider writing an ethical will to pass down values and life lessons alongside financial assets.

References

[1] – https://www.investopedia.com/retiring-this-year-ditch-the-4-rule-and-use-these-strategies-to-make-your-savings-last-8764124

[2] – https://blog.massmutual.com/retiring-investing/roth-ira-conversion-ladder

[3] – https://www.osc.ny.gov/retirement/publications/straight-talk-about-financial-planning-your-retirement

[4] – https://www.forbes.com/councils/forbesfinancecouncil/2024/05/02/when-is-it-time-to-hire-a-financial-planner/

[5] – https://www.aarp.org/caregiving/financial-legal/info-2021/understanding-long-term-care-insurance.html

[6] – https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/methods-maximize-tax-loss-harvesting-success.html

[7] – https://www.forbes.com/sites/jamiehopkins/2024/03/28/study-uncovers-opportunities-for-using-housing-wealth-in-retirement/

[8] – https://www.bankrate.com/retirement/maximize-your-social-security-benefits/

[9] – https://www.kiplinger.com/retirement/how-to-protect-your-retirement-from-sequence-of-returns-risk

[10] – https://www.ssa.gov/oact/quickcalc/spouse.html

[11] – https://www.kiplinger.com/retirement/want-to-retire-happily-plan-for-leisure-and-purpose

[12] – https://investor.vanguard.com/investor-resources-education/portfolio-management/diversifying-your-portfolio

[13] – https://www.kiplinger.com/retirement/digital-estate-planning-guide-for-digital-assets

[14] – https://www.usbank.com/wealth-management/financial-perspectives/trust-and-estate-planning/digital-estate-plan.html

[15] – https://www.irafinancialgroup.com/learn-more/financial-success/retirement-portfolio-diversification/

[16] – https://teamfallico.com/blog/real-estate-and-retirement-planning-a-smart-strategy-for-your-golden-years/

[17] – https://medium.com/due/the-role-of-real-estate-in-your-retirement-plan-due-6cf5244c97bb

[18] – https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/tuning-frequency-for-rebalancing.html

[19] – https://www.investopedia.com/how-roth-conversion-ladder-works-5214808

[20] – https://www.northwesternmutual.com/life-and-money/roth-conversion-ladder/

[21] – https://www.schwab.com/learn/story/how-to-cut-your-tax-bill-with-tax-loss-harvesting

[22] – https://www.whitecoatinvestor.com/what-is-geographic-arbitrage/

[23] – https://www.sdfoundation.org/news-events/sdf-news/maximizing-tax-benefits-of-charitable-giving-during-your-retirement/

[24] – https://www.fidelitycharitable.org/guidance/charitable-tax-strategies/charitable-contributions.html

[25] – https://www.investopedia.com/articles/personal-finance/012516/how-hire-retirement-advisor.asp

[26] – https://www.actec.org/estate-planning-essentials/retirement-legal-planning-considerations/

[27] – https://falcoandassociatespc.com/estate-planning-attorney/how-an-estate-plan-factors-into-your-retirement-plan-key-considerations/

[28] – https://colleenweber.com/could-a-retirement-tax-advisor-help-you-unlock-the-retirement-of-your-dreams/

[29] – https://www.cnbc.com/select/when-should-you-hire-a-financial-planner-/

[30] – https://tenonfinancial.com/

[31] – https://www.forbes.com/sites/robertberger/2023/10/01/5-alternatives-to-the-4-retirement-withdrawal-rule/

[32] – https://www.kitces.com/blog/dynamic-retirement-spending-small-but-permanent-variable-adjustments/

[33] – https://savantwealth.com/savant-views-news/article/rethinking-retirement-moving-past-the-4-rule/

[34] – https://www.cnbc.com/2023/10/26/the-connection-between-mental-health-and-retirement-emergency-savings.html

[35] – https://www.tfah.org/report-details/prevention-for-a-healthier-america/

[36] – https://jech.bmj.com/content/71/8/827

[37] – https://www.ncoa.org/article/when-should-you-start-investing-in-long-term-care-insurance/

[38] – https://www.ncoa.org/article/new-law-will-help-older-americans-save-for-retirement-access-mental-health-care/

[39] – https://money.usnews.com/money/retirement/aging/articles/retirement-destinations-overseas-with-excellent-health-care

[40] – https://pmc.ncbi.nlm.nih.gov/articles/PMC5296930/

[41] – https://www.fidelity.com/learning-center/smart-money/good-debt-vs-bad-debt

[42] – https://www.rbcwealthmanagement.com/en-ca/insights/borrow-to-invest-the-ups-and-downs-of-leverage-in-your-portfolio

[43] – https://www.schwab.com/learn/story/leveraging-your-assets-to-manage-your-wealth

[44] – https://www.aarp.org/social-security/claiming-strategies-for-couples/

[45] – https://www.schwab.com/learn/story/social-security-is-taxable-how-to-minimize-taxes

[46] – https://www.aarp.org/money/personal-finance/emergency-fund-mistakes-to-avoid/

[47] – https://www.nasdaq.com/articles/heres-how-much-retirees-should-keep-emergency-fund

[48] – https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/mitigating-sequence-of-return-risk/

[49] – https://www.citizensbank.com/learning/financial-goals-with-heloc.aspx

[50] – https://edrempel.com/money123-article-using-a-credit-line-as-your-emergency-fund/

[51] – https://www.health.harvard.edu/blog/will-a-purpose-driven-life-help-you-live-longer-2019112818378

[52] – https://www.medicalnewstoday.com/articles/longevity-having-a-purpose-may-help-you-live-longer-healthier

[53] – https://umra.hr.umich.edu/retire-thrive/

[54] – https://www.gcfretirement.com/blog/the-art-of-semi-retirement-balancing-work-and-leisure-in-the-next-chapter

[55] – https://www.ncsl.org/financial-services/elderly-financial-exploitation-legislation

[56] – https://www.actec.org/resource-center/video/how-to-talk-with-your-family-about-estate-planning/

[57] – https://flourishwealthmanagement.com/resources/blog/beyond-wealth-crafting-a-legacy-plan-with-purpose-and-passion/

[58] – https://www.outlookmoney.com/retirement/plan/succession/you-are-not-just-your-wealth-leaving-a-legacy-beyond-just-financial-assets