These figures might look daunting. I’ve dedicated my career to helping people create retirement savings strategies that deliver results.

A startling fact stands out: only 30% of Americans have mapped out their retirement finances. My experience as a financial advisor shows how this missing roadmap can shatter retirement dreams. A retired couple needs about $315,000 just to cover healthcare costs today.

These figures might look daunting. I’ve dedicated my career to helping people create retirement savings strategies that deliver results. The math tells an amazing story – a monthly investment of $50 over 40 years at a 7% return could build up to more than $130,000.

Here’s the bright side. Proven strategies exist to secure your retirement, regardless of where you are in your career journey. Your options range from maximizing your employer’s 401(k) match (which reaches $23,000 annually in 2024) to learning about tax-advantaged accounts. I’ll guide you through 10 practical steps that can reshape your retirement future.

Together we can create your path to a secure retirement with strategies tailored to your specific situation and goals.

Start Early and Harness the Power of Compound Growth

Image Source: Wealthy Retirement

Time is your biggest ally when building retirement wealth. I’ve seen with my own eyes how starting early can change your retirement savings through compound growth’s magic.

The Mathematical Advantage of Time in Retirement Savings

Let’s look at this eye-opening example: investing $1,000 at age 20 and letting it grow over 50 years gives you more than $29,458 through compound interest [1]. You could reach $990,000 by age 65 if you invest $550 monthly starting at age 30 with a 7% annual return [2]. Starting this same investment at age 45 leaves you with only $285,000 [2].

Compound growth shows its true power when your original investments create returns that earn extra returns. To name just one example, a $1,050 investment with 5% annual returns grows to $1,102.50 in year two and $1,157.63 in year three [3]. On top of that, putting aside 10% to 15% of your income can build substantial wealth over time [2].

Case Studies: Early vs. Late Retirement Savers

Here are two ground examples that show different paths to retirement success:

Susan and Norman started their retirement experience in their mid-40s with less than $100,000 in net worth [4]. They retired early through disciplined saving and smart planning by:

- Maximizing their 401(k) contributions

- Living below their means

- Creating multiple income streams

- Paying off all debt, including their mortgage

Martha found that there was a way to plan for retirement at age 47 and built a $150,000 nest egg in just three years [5]. She succeeded by quickly using aggressive saving strategies and making smart investment choices.

Strategies for Young Professionals

Young professionals should follow these tested approaches:

Make use of your biggest advantage – time. Small contributions grow by a lot through compound interest. To cite an instance, see how investing $475 monthly starting at age 22 could grow to $2.37 million by age 67, with an 8% average annual return [4].

These key actions deserve your attention:

- Take full advantage of employer-sponsored retirement plans, especially matching contributions [2]

- Set up automatic investing to ensure steady savings [1]

- Think over both traditional and Roth retirement accounts for tax benefits [2]

- Keep a long-term point of view, focusing on time in the market rather than timing the market [2]

Note that starting early doesn’t need big money. A modest $100 monthly added to an original $5,000 investment earning 5% APY could reach $23,763 in ten years [5]. Young professionals should save 15% of their pre-tax income yearly, including employer matches [6].

Take Full Advantage of Employer-Sponsored Retirement Plans

Image Source: Slavic401k

Building long-term wealth becomes easier with employer-sponsored retirement plans. My experience as a financial advisor shows that people who learn to maximize these benefits end up with much bigger retirement savings.

Understanding Your Company’s 401(k) Options

The numbers tell an interesting story – 95% of companies now give employer contributions to retirement plans [7]. Your traditional 401(k) lets you make pre-tax contributions and cuts down your current taxable income. Some employers also give you the choice of Roth 401(k)s. You pay taxes upfront with these, but the money comes out tax-free when you retire.

Negotiating for Better Retirement Benefits

Job changes and performance reviews give you a chance to negotiate retirement benefits. You should look beyond just salary talks and ask about better retirement packages. Recent data shows that 31% of employees would rather have an employer-sponsored 401(k) than a pay raise [7]. Knowing you can negotiate retirement benefits could mean big gains over time.

Maximizing Employer Matching Contributions

Most employers match $0.50 for every dollar you put in, up to 6% of your pay [7]. Let’s break this down – if you make $60,000 a year, you could get up to $1,800 in matched contributions [8]. Some companies are even more generous. They match dollar-for-dollar on the first 3% and throw in $0.50 more on the next 2% of pay [7].

Here’s how to get the most from your retirement savings:

- Put in enough to get the full employer match

- Learn your plan’s matching formula

- Bump up contributions when your salary goes up

- Keep track of annual contribution limits ($23,500 in 2025) [9]

Vesting Schedules and Job Transitions

IRS rules set two main vesting schedules that determine when you own your employer’s contributions [6]:

- Cliff Vesting: You get 100% after three years, with nothing before that [10]

- Graded Vesting: Your ownership grows step by step over six years max [10]

Good news – 40% of people now get immediate vesting of employer matching contributions [7]. Your vesting status matters when switching jobs. Leave too early and you might lose unvested employer contributions [10].

You have four choices for your 401(k) during job changes [11]:

- Keep it with your old employer

- Move it to your new employer’s plan

- Roll it into an IRA

- Cash out (watch out for penalties)

Smart decisions about retirement plans come from knowing how they work. Your retirement savings can grow faster when you maximize employer matches and time your career moves right with vesting schedules in mind.

Utilize Tax-Advantaged Retirement Accounts Strategically

Image Source: Lewis CPA

Tax planning serves as the life-blood of building a solid retirement nest egg. My years as a financial advisor taught me that broadening retirement accounts with different tax treatments helps maximize wealth over time.

Balancing Traditional and Roth Accounts

These accounts follow different tax rules. Traditional IRA contributions lower your current taxable income, but you’ll pay taxes on withdrawals during retirement [12]. Roth accounts work differently – you fund them with after-tax dollars and get tax-free growth. The money comes out tax-free once you’re 59½ and have kept the account for five years [12].

The year 2025 keeps traditional IRA contributions fully deductible if your Modified Adjusted Gross Income (MAGI) stays below $126,000 (joint) and $79,000 (single) [13]. You might qualify for partial deductions until your income hits $146,000 (joint) or $89,000 (single) [13].

Backdoor Roth IRA Strategies for High Earners

High-income earners who earn too much for a Roth IRA can still benefit from the backdoor strategy. The process works like this:

- Open a traditional IRA

- Make a nondeductible contribution

- Convert it to a Roth IRA right away

- File Form 8606 to report it [2]

The contribution limit reaches $7,000 in 2025, plus an extra $1,000 for folks 50 and older [2]. All the same, watch out for the pro-rata rule – it might trigger unexpected taxes if you have other traditional IRA money [2].

Using HSAs as Triple-Tax-Advantaged Retirement Accounts

Health Savings Accounts (HSAs) shine with their triple tax benefit structure:

- Pre-tax contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses [4]

Individual coverage limits hit $4,300 while family coverage reaches $8,550 in 2025 [4]. People 55 or older can add $1,000 more as catch-up contributions [4].

HSA funds roll over each year, unlike Flexible Spending Accounts. This money grows tax-free throughout your retirement years [14]. After 65, you can use HSA money for non-medical costs without penalties – you just pay regular income tax [4].

Smart investors might want to let their HSA funds grow instead of spending them on current medical costs. A $1,000 HSA investment growing at 7% yearly could reach $7,612 after 30 years – all tax-free when used for qualified medical expenses [4].

Create a Personalized Asset Allocation Strategy

Image Source: Barbara Friedberg Personal Finance

A tailored asset allocation strategy creates the foundations of successful retirement planning. My experience as a financial advisor shows that your retirement goals become achievable when you understand your risk capacity and tolerance.

Risk Tolerance Assessment Techniques

Risk tolerance includes two distinct parts: your willingness to take risks and your capacity to handle financial uncertainty. A well-adjusted questionnaire helps determine your risk profile [3]. These assessments typically group investors into three main categories – aggressive, moderate, and conservative [3].

Your risk assessment should include these vital factors:

- Current financial situation and stability

- Time horizon until retirement

- Additional income sources

- Healthcare needs

- Family obligations

Age-Based Portfolio Adjustments

Traditional allocation methods recommend subtracting your age from 110 or 120 to find the right percentage of stocks in your portfolio [1]. Life expectancy increases have made it necessary to keep a more aggressive allocation longer [1].

A 65-year-old investor would have 35% in stocks using the conventional approach (100 minus age) [15]. The modern formula (110 minus age) suggests 45% in stocks, which could lead to better growth opportunities [15].

Rebalancing Strategies and Timing

Studies show that yearly portfolio rebalancing gives the best results for most investors [16]. This method lets you capture equity premiums while keeping transaction costs lower than more frequent adjustments [16].

These rebalancing methods have proven effective:

- Calendar-based: Reset your portfolio to target allocation yearly

- Threshold-based: Rebalance when allocations move beyond specific percentages

- Combined approach: Review annually and rebalance if deviation goes past predetermined limits [16]

Market volatility should not trigger frequent rebalancing because transaction costs usually rise during turbulent periods [16]. The focus should stay on keeping your target allocation through planned, systematic adjustments.

Success comes from following these rebalancing practices:

- Regular allocation monitoring without excessive trading

- Strategic use of portfolio cash flows

- Tax-smart asset selling decisions

- Disciplined approach during market swings [17]

Note that your asset allocation strategy must evolve with your changing circumstances. Life events, inheritance, or changes in retirement goals might require adjustments to your risk capacity [3]. Regular reviews and careful planning help maintain an allocation that matches both your risk tolerance and retirement objectives.

Protect Your Retirement Savings from Inflation

Image Source: Jon Luskin

Your retirement savings need protection against inflation through multiple strategies. Rising prices make it vital to use proven methods that help maintain your purchasing power throughout retirement.

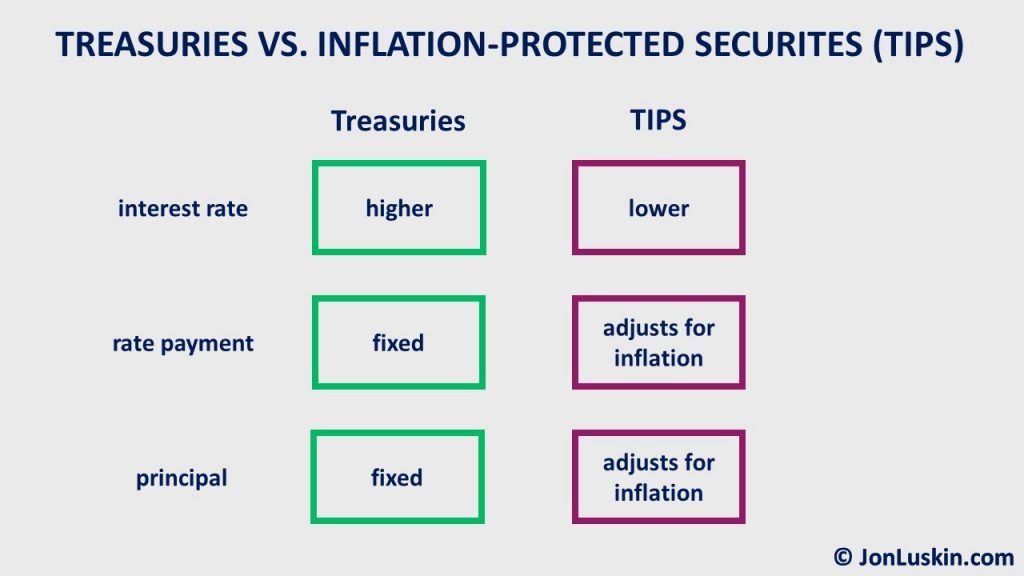

TIPS and I-Bonds in Retirement Portfolios

Treasury Inflation-Protected Securities (TIPS) provide a direct hedge against rising prices. These securities adjust their principal value based on changes in the Consumer Price Index [9]. Series I Savings Bonds are another tool among TIPS that fight inflation. Each Social Security number allows purchase limits of $10,000 yearly [18].

Both instruments give you specific advantages:

- TIPS guarantee inflation-adjusted returns when held to maturity [9]

- I-bonds combine fixed rates with inflation adjustments and currently return 4.28% [19]

- You won’t pay state and local taxes on earned interest [19]

Real Assets as Inflation Hedges

Traditional stock/bond portfolios become stronger against inflation by adding real assets. Portfolios with real assets showed an inflation beta of -1.3, while those without reached -2.1 [20]. This strategy delivered 62 basis points of outperformance and reduced volatility over the three-year period ending December 2023 [20].

Dividend Growth Investing for Inflation Protection

Dividend-paying stocks help fight inflation through steady income streams that grow over time [21]. Past data shows dividend growth went beyond 10% during previous inflationary periods, particularly in 1973, 1979, and the early 1990s [22].

The benefits are clear:

- Companies with strong pricing power pass increased costs to consumers

- Dividend payments grow with inflation naturally

- You get both income growth and capital appreciation

Adjusting Withdrawal Rates for Inflation

Your purchasing power depends on smart withdrawal strategies. The traditional 4% rule suggests taking no more than 4-5% of savings in your first retirement year. This amount should adjust yearly for inflation [23].

Here’s a practical example: starting with $100,000 annual withdrawals, two years of 7% inflation would push withdrawals to $114,490 by year three [24]. Regular review and adjustment of withdrawal rates become vital for long-term success.

Your retirement income strategy works better when you:

- Check portfolio performance and inflation trends yearly

- Change withdrawal rates based on market conditions

- Lower withdrawals during tough market periods

- Use a flexible spending approach that adapts to economic changes [25]

Leverage Catch-Up Contributions for Late Starters

Image Source: Meld Financial

Catch-up contributions are a game-changer for people nearing retirement age. My experience as a financial advisor shows how these special provisions have helped many late starters secure their retirement future.

Maximizing Age 50+ Catch-Up Options

The IRS lets you make extra contributions above standard retirement account limits after turning 50. Traditional and Roth IRA catch-up limits will be $1,000 in 2025, which brings total possible contributions to $8,000 [26]. Your 401(k) plans allow an additional $7,500 on top of the standard $23,500 limit, making the maximum $31,000 [27].

People with SIMPLE IRA plans can also benefit. Employees aged 50 and older can contribute an extra $3,850 in 2025 [28]. These contributions need to happen through elective deferrals before the plan year ends [29].

Super Catch-Up Strategies for Ages 60-63

A new provision coming in 2025 creates even better catch-up opportunities. Workers between 60-63 years old can put away up to $11,250 in their 401(k) plans – that’s $3,750 more than the standard catch-up amount [30]. SIMPLE plan participants in this age range get better limits too, reaching $5,250 [28].

New rules for catch-up contributions start in 2026 based on your income:

- You can keep making pre-tax contributions if you earn under $145,000

- Your catch-up amounts must go to Roth accounts if you earn more than $145,000 [27]

Accelerated Savings Techniques

You can boost your savings beyond catch-up provisions with these proven strategies:

Set up automatic contributions to make saving consistent. Most employer plans let you deduct pre-tax money straight from your paycheck [31]. Small business owners can also set up monthly automatic deductions to simplify their retirement savings.

Here’s a real-world example: Someone starting with no retirement savings at 40 who puts away $23,500 yearly for 25 years could build up $1.5 million, assuming 7% annual returns [7]. The numbers look even better at age 50 – maxing out both standard and catch-up contributions at $31,000 yearly could grow to nearly $800,000 in 15 years under similar conditions.

The best results come from coordinating contributions across your retirement accounts. A smart approach might include:

- Maxing out catch-ups in your employer-sponsored plan

- Adding money to both traditional and Roth IRAs when you qualify

- Using SIMPLE IRA catch-ups if you work for yourself

- Looking into HSA catch-up contributions at age 55 [32]

Implement Smart Debt Management Strategies

Image Source: Investopedia

Smart debt management is a vital part of building retirement wealth. My analysis of different debt strategies shows that the best financial outcomes come from balancing debt repayment with retirement savings.

Prioritizing Debt Payoff vs. Retirement Savings

Interest rates and employer benefits largely determine the choice between paying off debt and saving for retirement. Debts with rates above 10% need quick attention [8]. Stopping retirement savings completely to clear debt rarely works best. Studies show 36% of U.S. adults can handle both debt repayment and emergency savings at once [33].

Mortgage Strategies Near Retirement

Your mortgage strategy needs careful thought as retirement approaches. Fixed-rate mortgages give you predictable payments, unlike rent costs that keep changing [34]. Homeowners get two main benefits:

- They build equity through principal payments

- Their property value might grow over time

Baby boomers now carry more mortgage debt than earlier generations. The number of mortgage holders aged 75 and above jumped from 5% in 1995 to 25% in 2022 [35].

Student Loan Management for Retirement Savers

Student loans substantially affect retirement planning. Average monthly payments reach $393, while typical Social Security benefits are $1,907 [36]. Income-Driven Repayment (IDR) plans help by matching payments to your discretionary income. Federal loan consolidation can stretch repayment terms and might lower your monthly payments [36].

Using Good Debt to Boost Retirement Security

The difference between “good” and “bad” debt matters a lot. Good debt usually has these features:

- Lower interest rates

- Tax advantages

- Asset value growth potential

- Ways to generate income [37]

Your debt-to-income ratio is a vital metric. Experts say to keep this ratio under 36% [37]. Smart debt management follows the 28/36 rule: housing costs should stay under 28% of your pre-tax monthly income, and all debt payments under 36% [6].

These proven strategies work best:

- Keep emergency savings while paying debts

- Use debt consolidation when it helps

- Look into refinancing high-interest debts

- Match debt reduction with retirement contributions [10]

The plan should address both today’s obligations and tomorrow’s security. A strong foundation for retirement success comes from staying liquid while managing debt effectively [38].

Develop a Retirement Income Plan

Image Source: RetireGuide

A reliable retirement income is the life-blood of financial security in your golden years. Smart planning and good execution will help you build income streams that last throughout retirement.

The 4% Rule and Its Alternatives

The traditional 4% withdrawal rule gives you a starting point for retirement income planning. This approach suggests withdrawing 4% of your portfolio in the first year and adjusting that amount annually for inflation [39]. Research shows that dynamic spending strategies work better and might allow withdrawal rates up to 5% with proper planning [40].

Creating a Retirement Paycheck System

Building a dependable retirement paycheck means coordinating several income sources. Social Security creates the foundation and provides inflation-adjusted benefits that grow when you delay claiming until age 70 [41]. Your retirement plan should include:

- Pension payments that guarantee lifetime income

- Investment withdrawals from retirement accounts

- Annuities that provide protected income streams [42]

Bucket Strategies for Retirement Income

The bucket approach splits your retirement assets into three timeframes:

- Short-term bucket: 1-3 years of expenses in cash or low-risk investments [11]

- Medium-term bucket: 3-10 years of funds in balanced investments [43]

- Long-term bucket: Growth investments for expenses beyond 10 years [44]

This strategy helps you handle market downturns because your money spreads across multiple investment accounts with different risk levels and liquidity [11].

Guaranteed Income Sources and Their Role

Guaranteed income delivers essential financial stability throughout retirement. Social Security remains the most common form and provides simple income for basic expenses [41]. Annuities give you extra guaranteed income through:

- Fixed payments for life

- Protection from market fluctuations

- Optional benefits for spouse coverage [41]

Your retirement strategy should include income from various sources, even with pension income [41]. Good coordination of these income streams creates a balanced approach that provides security and growth potential throughout retirement [45].

Prepare for Healthcare Costs in Retirement

Image Source: Business Wire

Healthcare expenses are a major financial challenge that retirees face. A 65-year-old couple retiring today needs about $315,000 to cover medical expenses, not including long-term care costs [46].

Estimating Your Healthcare Expenses

The average 65-year-old woman’s healthcare costs start at $5,100 annually [47]. These costs rise steadily with age. People aged 65-74 spend $13,000 yearly, while those over 85 spend up to $40,000 [48]. Medicare premiums, deductibles, and out-of-pocket expenses make up most of these costs [47].

Medicare Planning and Supplemental Insurance

Original Medicare doesn’t cover every healthcare cost [13]. Medigap, a supplemental insurance, helps bridge these coverage gaps [49]. Here’s what you need to know about Medicare coverage:

- Sign up during your 7-month original enrollment period

- Think over both Medicare Parts A, B, and D

- Review Medicare Advantage plans to get complete coverage

- Look into Medigap policies for extra protection [50]

Long-Term Care Funding Options

Long-term care needs special attention because people turning 65 today have almost a 70% chance of needing these services [13]. Private nursing home care costs about $8,800 each month [47]. These funding options can help:

- Long-term care insurance

- Hybrid life insurance policies with care benefits

- Health Savings Accounts (HSAs)

- Personal savings and investments [51]

Health-Focused Investments

HSAs are valuable because of their triple tax benefit structure [47]. The contribution limits for 2025 reach $4,300 for individual coverage and $8,550 for family coverage. People 55 and older can add an extra $1,000 catch-up contribution [50].

Emergency funds are vital too. You should save enough to cover your maximum yearly out-of-pocket expenses [52]. Smart investors also put money into growth assets that have historically beaten medical inflation rates [52].

Adjust Your Strategy Through Regular Financial Reviews

Image Source: Investopedia

Regular reviews are the life-blood of a successful retirement strategy. My experience shows that checking your plans periodically helps them adapt to changing circumstances and market conditions.

Annual Retirement Plan Checkups

You should review your retirement investments at least once yearly, and more often as retirement approaches [53]. Beyond simple portfolio monitoring, let’s get into these key elements:

- Investment performance and fees

- Asset allocation arrangement

- Contribution levels versus goals

- Tax implications of current strategies

Life Event Adjustments to Your Retirement Strategy

Life changes often require modifications to retirement plans. Parents spend about $240,000 to raise a child to age 18, which affects retirement savings capacity [2]. These significant events need strategy adjustments:

- Marriage or divorce

- Starting a family

- Job changes or promotions

- Relocation

- Health status changes

Working with Financial Professionals

Professional guidance is valuable – 64% of retirees say personal consultations helped improve their financial knowledge effectively [54]. Financial advisors excel at:

- Navigating complex investment options

- Creating strategies for specific goals

- Explaining ways to maximize savings

- Coordinating retirement benefits

Using Technology to Track Retirement Progress

Technology makes it easier to monitor retirement progress. Digital tools come with features like:

- Immediate portfolio tracking

- Automated contribution scheduling

- Investment performance analysis

- Goal progress visualization

Several retirement planning platforms provide complete services. Betterment offers automated portfolio management and goal tracking [55]. The platform makes shared account linking possible to analyze savings, net worth, and spending patterns [55]. These tools include retirement calculators that help assess savings adequacy and project future needs.

Note that security measures matter when using financial technology. Most apps implement strong protection for personal information [56]. The combination of professional guidance and technological tools creates a balanced approach to retirement planning oversight.

Comparison Table

| Strategy | Key Benefits | Implementation Timeline | Specific Numbers/Limits (2025) | Notable Considerations |

|---|---|---|---|---|

| Start Early and Use Compound Growth | Major effect on wealth building through compound interest | Long-term (40+ years ideal) | $550/month at age 30 can reach $990,000 by 65 | Small contributions of $100/month can grow substantially over time |

| Maximize Employer Plans | Pre-tax contributions and employer matching | Right after starting employment | Contribution limit: $23,500 ($31,000 with catch-up) | 95% of companies offer employer contributions |

| Use Tax-Advantaged Accounts | Tax benefits across different account types | Throughout your career | IRA limit: $7,000 (+$1,000 catch-up), HSA: $4,300 individual/$8,550 family | High earners should look into backdoor Roth options |

| Build Custom Asset Allocation | Better risk management and portfolio results | Regular portfolio updates needed | 110-age formula for stock allocation percentage | Yearly rebalancing gives optimal results |

| Guard Against Inflation | Keeps buying power strong over time | Regular monitoring needed | I-bonds current return: 4.28% | Mix TIPS, real assets, and dividend growth stocks |

| Use Catch-Up Contributions | Extra savings options for older workers | Age 50+ | 401(k) catch-up: $7,500, IRA catch-up: $1,000 | Higher limits for ages 60-63 ($11,250) |

| Apply Smart Debt Management | Balance debt payoff with savings | Regular assessment needed | Recommended debt-to-income ratio: below 36% | Pay off high-interest debt while saving for retirement |

| Create Retirement Income Plan | Smart withdrawal approach | Plan before retirement | 4-5% starting withdrawal rate | Bucket strategy works well for different time periods |

| Plan for Healthcare Costs | Protection from big medical bills | Plan before retirement | $315,000 estimated for retired couple at 65 | Look into HSA and long-term care insurance |

| Review Finances Regularly | Keeps strategy matched to goals | Check yearly at minimum | N/A | Update based on life changes and markets |

Closing Thoughts

My years of helping clients build their retirement nest eggs have taught me these ten strategies really work. Each approach, from maximizing employer matches to protecting against inflation, creates lasting financial security.

Success comes from making these strategies your own. Starting early works best, but smart planning can strengthen anyone’s retirement outlook. A simple step like contributing $550 monthly at age 30 could grow to $990,000 by retirement age.

Your retirement planning needs change as your life does. Regular reviews help your strategy adapt to new goals and market conditions. You’ll need to focus more on healthcare costs, inflation protection, and income planning as retirement gets closer.

Want more retirement planning insights and updates on the latest financial strategies? Visit trendnovaworld.com. We share practical tips to help secure your financial future.

These proven approaches have helped countless people achieve their retirement dreams. The process might seem complex, but taking it step by step makes success possible. Start using these strategies today. You’ll feel confident knowing you’re actively building your retirement future.

Keep Learning! Explore These Valuable Blogs:

• 🏠 How to Master Working from Home – Entrepreneurs Are Winning in 2025 (Real Data Inside)

• 🤖 Mastering Fully Automated Websites – My 2025 Experience

• 🎨 My Top UI/UX Design Tools for AR & VR Interfaces in 2025

• 🌐 Discover the Best Web Hosting for Your AI-Powered Website in 2025

FAQs

Q1. What are the retirement savings contribution limits for 2025? For 2025, the contribution limit for 401(k), 403(b), and similar plans is $23,500 for individuals under 50. Those 50 and older can make an additional $7,500 catch-up contribution, bringing their total limit to $31,000.

Q2. How much savings do I need to generate $1,000 in monthly retirement income? According to the $1,000 a month rule, you should aim to have about $240,000 saved for every $1,000 of monthly retirement income you want to generate. This guideline can help estimate the savings needed for sustainable retirement income.

Q3. What is the average 401(k) balance for a 65-year-old? Based on data from Vanguard, the average 401(k) balance for those 65 and older is $272,588. However, the median balance of $88,488 may be a more accurate representation of the typical balance, as it’s not skewed by a few very large accounts.

Q4. Is it possible to retire at 62 with $400,000 in a 401(k)? Retiring at 62 with $400,000 in a 401(k) can generate a livable income, depending on your portfolio structure and chosen location. However, while this amount can provide basic needs, it may not ensure a comfortable retirement without additional income sources or careful budgeting.

Q5. How can I protect my retirement savings from inflation? To protect your retirement savings from inflation, consider diversifying your portfolio with inflation-resistant investments. This may include Treasury Inflation-Protected Securities (TIPS), I-Bonds, real assets, and dividend growth stocks. Regular portfolio reviews and adjustments can also help maintain purchasing power over time.

References

[1] – https://www.sofi.com/learn/content/asset-allocation-by-age/

[2] – https://www.northamericancompany.com/plan-for-tomorrow/when-to-reassess-a-retirement-plan

[3] – https://www.firstcitizens.com/personal/insights/retirement/retirement-risk-assessment

[4] – https://www.fidelity.com/viewpoints/wealth-management/hsas-and-your-retirement

[5] – https://www.bankrate.com/banking/savings/compound-savings-calculator/

[6] – https://www.ameripriseadvisors.com/team/bordelon-retirement-planning-group/insights/effective-debt-management/

[7] – https://www.citizensbank.com/learning/retirement-catch-up-strategies.aspx

[8] – https://www.principal.com/individuals/build-your-knowledge/7-steps-pay-debt-and-save-retirement

[9] – https://www.pimco.com/us/en/resources/education/understanding-treasury-inflation-protected-securities

[10] – https://www.debt.org/retirement/prioritize-savings-vs-payoff/

[11] – https://www.usbank.com/retirement-planning/financial-perspectives/managing-retirement-during-market-downturns.html

[12] – https://www.northwesternmutual.com/life-and-money/tax-planning-strategies-for-retirement/

[13] – https://www.fidelity.com/viewpoints/personal-finance/long-term-care-costs-options

[14] – https://www.morganstanley.com/atwork/employees/learning-center/articles/hsa-retirement-savings

[15] – https://www.kiplinger.com/retirement/risk-in-retirement-what-level-works-for-you

[16] – https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/tuning-frequency-for-rebalancing.html

[17] – https://investor.vanguard.com/investor-resources-education/portfolio-management/rebalancing-your-portfolio

[18] – https://retirementresearcher.com/every-retiree-know-bonds/

[19] – https://money.usnews.com/money/retirement/articles/are-i-bonds-a-good-investment-for-retirees

[20] – https://www.pimco.com/us/en/insights/real-assets-bolstering-portfolios-as-inflation-lingers

[21] – https://www.forbes.com/sites/investor-hub/article/best-dividend-stocks-to-hedge-inflation/

[22] – https://www.dividend.com/how-to-invest/dividends-an-inflation-hedge/?utm_source=Dividend.com&utm_campaign=8b9ca18a61-ExpTrial_Engage_Content_Dispatch_8_10_2017&utm_medium=email&utm_term=0_5465108463-8b9ca18a61-48011021&goal=0_5465108463-8b9ca18a61-48011021

[23] – https://www.fidelity.com/viewpoints/retirement/how-long-will-savings-last

[24] – https://www.kiplinger.com/retirement/retirement-planning/the-4-rule-gets-a-closer-look

[25] – https://retirement.johnhancock.com/us/en/participant/a-guide-for-job-changers-and-retirees/your-retirement-withdrawal-strategy-four-tips-for-managing-inflation

[26] – https://slavic401k.com/retirement-savings-for-late-starters/

[27] – https://www.schwab.com/learn/story/what-to-know-about-catch-up-contributions

[28] – https://smartasset.com/retirement/5-retirement-planning-moves-for-late-starters

[29] – https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-catch-up-contributions

[30] – https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000

[31] – https://www.finra.org/investors/insights/things-to-do-boost-retirement-savings

[32] – https://www.fidelity.com/viewpoints/retirement/catch-up-contributions

[33] – https://www.bankrate.com/banking/savings/these-guidelines-will-help-you-decide-whether-to-pay-down-debt-or-save/

[34] – https://www.cnbc.com/2024/08/27/financial-experts-view-your-mortgage-as-part-of-your-retirement-plan.html

[35] – https://www.investopedia.com/articles/financial-advisors/011315/should-retirees-pay-their-mortgage.asp

[36] – https://www.empower.com/the-currency/money/managing-student-loan-debt-retirement

[37] – https://www.planmember.com/the401kgroup/build-wealth-using-debt/

[38] – https://newsroom.wiley.com/press-releases/press-release-details/2015/The-Value-of-Debt-in-Retirement-1aa0703c7/default.aspx

[39] – https://www.forbes.com/sites/robertberger/2023/10/01/5-alternatives-to-the-4-retirement-withdrawal-rule/

[40] – https://investor.vanguard.com/investor-resources-education/article/retirement-withdrawal-strategies

[41] – https://www.corebridgefinancial.com/insights-education/sources-of-guaranteed-income

[42] – https://www.tiaa.org/public/learn/lifetime-income

[43] – https://www.schwab.com/learn/story/phasing-retirement-with-bucket-drawdown-strategy

[44] – https://www.rbcgam.com/en/ca/learn-plan/retirement-resources/how-to-create-a-sustainable-retirement-income/detail

[45] – https://realinvestmentadvice.com/resources/blog/retirement-income-planning/

[46] – https://institutional.fidelity.com/advisors/insights/spotlights/retirement-income-planning/retirement-planning-health-care-costs

[47] – https://corporate.vanguard.com/content/dam/corp/research/pdf/Planning-for-health-care-costs-in-retirement-US-ISGPLHC_072021_Online.pdf

[48] – https://www.rbcwealthmanagement.com/en-us/insights/the-real-cost-of-health-care-in-retirement

[49] – https://www.medicare.gov/health-drug-plans/medigap

[50] – https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

[51] – https://www.bairdwealth.com/insights/wealth-management-perspectives/2024/06/how-to-pay-for-long-term-care/

[52] – https://www.investors.com/etfs-and-funds/personal-finance/retirement-health-care-costs/

[53] – https://investor.vanguard.com/investor-resources-education/retirement/planning

[54] – https://www.athene.com/smart-strategies/will-technology-affect-your-retirement-planning.html

[55] – https://money.usnews.com/money/retirement/401ks/articles/best-retirement-planning-tools-and-software

[56] – https://dechtmanwealth.com/insights/blog/how-to-use-technology-to-monitor-your-retirement-savings