The numbers might surprise you – a retired couple needs about $315,000 just to cover their medical expenses in retirement. This figure seems staggering, and it represents just one part of the retirement spending puzzle.

The numbers might surprise you – a retired couple needs about $315,000 just to cover their medical expenses in retirement. This figure seems staggering, and it represents just one part of the retirement spending puzzle.

My experience shows that retirees often struggle with retirement budgeting. The average Social Security payment of $1,867 per month doesn’t cover simple needs. The reality hits harder when you consider that retirees typically spend $54,975 each year on household expenses. This includes $11,186 for shelter and $7,505 for healthcare.

My background as a financial writer in retirement planning leads me to suggest replacing 70-80% of your pre-retirement income to keep your current lifestyle. This goal needs smart retirement budget planning and effective money-saving strategies. These 15 practical tips will help you stretch your retirement savings and make your money last longer.

Create a Retirement Budget Baseline

Image Source: Retirement Budget Calculator

A solid retirement budget begins with understanding your financial baseline. My experience shows that most retirees need between 54% to 87% of their pre-retirement income to maintain their lifestyle [1].

Calculating Your Retirement Income Ratio

Your retirement income ratio calculation should start with an analysis of your current monthly expenses. To cite an instance, if your pre-retirement income is $45,000, plan to spend approximately $36,000 annually in retirement [2]. All the same, this ratio should change based on your specific circumstances. People with higher incomes usually need a smaller percentage of their working income for retirement [2].

Essential vs. Discretionary Spending Categories

Breaking down expenses into essential and discretionary categories are the foundations of an eco-friendly retirement budget. Essential expenses cover:

- Housing costs and property taxes

- Healthcare insurance and out-of-pocket expenses

- Simple transportation

- Food and utilities

- Insurance premiums [3]

Discretionary spending includes activities that boost your retirement lifestyle, such as travel, hobbies, and entertainment. Research shows that these discretionary activities, especially travel and dining out, bring the most life satisfaction to retirees [4].

Setting Realistic Spending Targets

Rough estimates won’t cut it. You should track your actual spending patterns for several months before retirement. On top of that, set aside approximately 1-5% of your home’s value as a repair reserve [4]. A typical 65-year-old couple should budget around $330,000 for expected medical expenses through their life expectancy [2].

Financial flexibility improves when you express your discretionary spending as a range instead of a fixed amount [3]. You should allocate at least 15% of your retirement budget specifically for healthcare expenses [2]. A monthly spending plan should line up with your expected retirement income sources, such as Social Security, pensions, and investment withdrawals [3].

These baseline metrics and regular reviews will position you better to make informed decisions about your retirement spending. Note that you should factor in both routine expenses and occasional large purchases, such as replacing appliances or buying a new car [3].

Match Fixed Expenses to Guaranteed Income

Image Source: Western & Southern Financial Group

A stable retirement income begins when you match your fixed expenses to guaranteed income sources. My analysis of retirement planning strategies shows this method builds a solid foundation for long-term financial security.

Identifying Your Guaranteed Income Sources

Social Security stands as the most common guaranteed income source that provides steady monthly payments and increases with inflation [2]. Pensions offer another reliable income stream based on your work history and earnings, though they’re less common now [5]. Fixed annuities give you guaranteed rates of return over specific periods as a third option [6].

Calculating Your Essential Expense Coverage

Your fixed expenses should match your guaranteed income streams. Your monthly Social Security benefit might cover simple utilities and groceries – that’s a good start. Recent data shows Social Security benefits help 73% of Americans handle their monthly retirement costs [6]. You might want to buy an annuity to fill gaps between essential expenses and guaranteed income [7].

Strategies for Closing Income Gaps

You can try these strategies when guaranteed income isn’t enough:

- Wait until age 70 to claim Social Security benefits for maximum payments [8]

- Turn retirement savings into extra guaranteed income through annuities [6]

- Work part-time during early retirement [5]

- Pay off debt or downsize before retirement to cut fixed expenses [7]

Creating a Fixed Expense Safety Net

A dedicated emergency fund for fixed expenses provides vital protection. You should keep 6-8 months of essential expenses in available accounts [2]. This safety net helps you handle unexpected costs without disrupting your regular retirement budget.

Research shows people who add annuity income to their retirement strategy feel more confident – 74% feel sure about maintaining comfortable retirement living standards [4]. Retirees who have guaranteed income sources report higher life satisfaction and spend more time on activities they enjoy [4].

Matching fixed expenses to guaranteed income creates a stable foundation for retirement spending. This strategy lets you use variable income sources, such as investment withdrawals, for lifestyle choices and discretionary expenses [5].

Implement the 4% Withdrawal Rule Strategically

Image Source: AOL.com

Retirement planning in 2025’s economic world needs a fresh look at the traditional 4% withdrawal rule. Market analysis suggests a 3.7% starting withdrawal rate that helps your retirement savings last through 30 years [9].

Understanding the 4% Rule in Today’s Economy

A classic retirement approach lets you withdraw 4% of your investment balance in your first retirement year and adjust that amount yearly for inflation [10]. Your $500,000 nest egg would yield $20,000 as your original withdrawal [10]. Current market conditions and higher volatility make this traditional approach need some tweaking.

Adjusting Withdrawals Based on Market Performance

Rather than sticking to the 4% rule, you could make these market-based adjustments:

- Skip inflation adjustments after negative portfolio returns

- Lower withdrawals during major market downturns

- Make conservative increases during strong market performance

A dynamic withdrawal strategy substantially improves your portfolio’s longevity. Retirees who use this approach with a 50-year retirement horizon boost their success rate from 36% to 56% [11].

Creating a Flexible Withdrawal Strategy

“Guardrails” method provides a practical framework to flexible withdrawals. This approach helps you:

- Set original withdrawal boundaries

- Boost spending by inflation plus 10% in good markets

- Cut spending by 10% during market downturns [12]

A dynamic spending strategy boosts your retirement success probability from 56% to 90% over 50 years [11]. Investment fees are vital – portfolios with 0.2% expense ratio maintain 28% success rate, while 1% fees drop it below 9% [11].

Flexibility remains the cornerstone of success. Regular portfolio reviews and market-based adjustments work better than rigid withdrawal schedules to create lasting retirement income. A financial advisor can help tailor this approach to your risk tolerance and specific situation.

Budget for Healthcare with a Three-Tier Approach

Image Source: RetireGuide

Healthcare costs represent one of the biggest financial hurdles you’ll face in retirement. My research shows a budget-friendly three-tier strategy helps you manage these expenses and protects your retirement savings.

Routine Medical Expense Planning

Medicare covers approximately two-thirds of medical costs in retirement [3]. A typical 65-year-old couple needs to set aside $330,000 for medical expenses, not counting long-term care [3]. You can manage routine costs by:

- Budgeting for Medicare premiums, copays, and deductibles

- Adding supplemental insurance to cover gaps

- Getting prescription drug coverage through Medicare Part D

Managing Chronic Condition Costs

Chronic conditions substantially affect retirement healthcare spending. Diabetes costs average $20,137 per person each year, while Alzheimer’s and dementia-related expenses reach $48,701 annually [1]. Older women bear much of the financial burden and make up two-thirds of those with the highest yearly medical costs [1].

Preparing for Catastrophic Health Events

A catastrophic illness can drain your retirement savings quickly. Most insurance plans cap lifetime benefits between $250,000 to $1 million [13]. You can protect yourself against major health events by:

- Keeping emergency medical funds ready

- Checking insurance coverage limits yearly

- Looking into high-deductible health plans with health savings accounts

Long-Term Care Considerations

People turning 65 today have about a 70% chance of needing long-term care services [14]. Current costs run high:

- Private nursing home room: $10,025 monthly

- Assisted living facility: $5,511 monthly

- Home health aide: $213 daily [15]

Regular health insurance and Medicare rarely cover long-term care expenses [14]. Learning about long-term care insurance in your 40s, 50s, or 60s is vital since premiums stay lower and qualification chances remain higher during these years [15].

This three-tier approach positions you better to handle healthcare expenses throughout retirement. Working with a financial advisor helps create a complete strategy that fits your health needs and financial situation [14].

Automate Your Bill Payments and Savings

Image Source: SoFi

Retirees can reduce their stress and streamline money management by automating their financial tasks. My years of helping retirees optimize their budgets show that automatic systems are vital to maintain financial stability.

Setting Up a Retirement Bill Payment System

Electronic payments give you many advantages over traditional methods. Electronic payments process quickly and provide immediate confirmation [16]. Automatic payments remove the risk of missed deadlines or lost checks, which cost nearly eight times more to process than electronic transactions [16]. Your payments will process on time without manual tracking when you schedule them for specific dates [16].

Creating Automatic Transfers for Discretionary Spending

Your spending discipline improves with automatic transfers between accounts. You should think over allocating specific amounts to different savings goals through scheduled transfers [17]. This “set it and forget it” approach builds consistent saving habits without extra effort [17]. Money moves straight to savings through automated transfers, which helps limit impulsive spending [18].

Using Alerts to Prevent Overspending

Low balance alerts are a great way to get protection against overspending. Recent data shows 31% of retirees spend more than they can afford [19]. You can get up-to-the-minute updates when accounts reach preset limits by setting up customized alerts through your bank’s app or website [20]. These notifications help you avoid overdraft fees and declined transactions while staying within budget [20].

Digital Tools for Financial Automation

Digital tools have transformed modern retirement planning. Robo-advisors analyze your financial situation and goals to create suitable investment strategies [6]. Mobile apps let you track accounts, investments, and spending patterns completely [6]. Most financial institutions now provide integrated platforms where you can monitor retirement accounts, adjust contribution levels, and view retirement projections [4].

These automation strategies will give you better control over retirement finances while reducing manual money management time. Of course, regular monitoring matters – quarterly reviews help arrange your automated systems with changing needs and goals [21].

Adopt the ‘Go-Go, Slow-Go, No-Go’ Budget Framework

Image Source: Kiplinger

A realistic retirement budget needs a good grasp of spending patterns. My analysis of retirement spending data shows three clear phases that shape how we should plan our finances.

Budgeting for Your Active Early Retirement Years

The “Go-Go” years cover your first decade of retirement. You’ll likely spend more and live an active lifestyle during this time. Many retirees keep spending at pre-retirement levels or sometimes even more [22]. Travel costs hit their peak and become the third-biggest expense for retirees [23]. Your health is usually at its best during this phase, making it perfect to check off your bucket list items [24].

Transitioning to Mid-Retirement Spending Patterns

The “Slow-Go” phase typically starts in your mid-to-late 70s. Your activity levels drop and priorities change naturally. The yearly spending usually goes down by about 2% during this time [25]. Local entertainment and community activities replace long trips. Healthcare costs start to climb steadily, but daily living expenses tend to fall [26].

Planning for Later Retirement Needs

The “No-Go” years begin around your early 80s and bring big changes to how you spend. Healthcare becomes your biggest expense. Assisted living facilities cost about $5,511 monthly while private nursing care runs up to $10,025 per month [25]. You might spend less on other things, but medical costs usually rise faster than inflation during this phase [22].

Adjusting Your Budget Between Phases

Your long-term financial success depends on flexibility between phases. Here are some phase-specific changes to think over:

- Save extra money for leisure and travel in early retirement [24]

- Build up reserves for growing medical costs in later years [26]

- Check your investment portfolios often to match your changing needs [22]

Research shows that while overall expenses drop through retirement, they stay steady once you factor in inflation [25]. Understanding these different phases helps you prepare better for what’s ahead. You can create a more realistic retirement budget that grows with your lifestyle needs.

Consolidate and Simplify Financial Accounts

Image Source: Continuum Wealth

Managing multiple retirement accounts creates needless complexity. My research into retirement account management strategies shows that a simpler financial portfolio is key to better retirement planning.

Benefits of Account Consolidation

Bringing retirement accounts together has clear advantages. Merging multiple accounts cuts down on yearly fees and administrative charges [27]. Your combined larger account balance often qualifies you for lower fees [28]. A united account gives you a better view of your asset allocation and helps prevent overlapping investments [28].

Step-by-Step Account Simplification Process

Start by making a list of all your retirement accounts and what they’re for [8]. Then assess each account’s fees, including what you pay for administration, management, and service [8]. These transfer options might work for you:

- Direct transfers between similar account types (unlimited annually)

- Rollovers between different account types (IRS limits apply)

- Direct rollovers to avoid 60-day transfer windows and potential penalties [28]

Choosing the Right Financial Institutions

Pick providers based on investment options, fee structures, and service quality. Look for institutions that offer good digital tools to manage your accounts [29]. Check their retirement planning history, investment options, and tech capabilities [29]. Many providers now blend platforms that let you watch your retirement accounts, change contributions, and see retirement projections [29].

Maintaining Financial Organization

Good organization goes beyond the original consolidation. Check your beneficiary designations often, especially once you turn 73 when Required Minimum Distributions (RMDs) start [28]. A united account makes RMD calculations easier and helps you avoid big tax penalties for missed withdrawals [28]. Your estate planning becomes simpler too, as executors and heirs have fewer hurdles to jump [28].

These account consolidation strategies help you take better control of your retirement finances. A simpler account setup gives you more time to focus on investment strategies and retirement goals [30]. You can rebalance and track your progress easily when everything’s in one place [30].

Create a Sustainable Travel Budget

Image Source: Trip Of A Lifestyle

Travel expenses rank among the top priorities when planning for retirement. My analysis of retirement travel patterns shows that a sustainable budget needs to balance dreams with financial realities.

Affordable Travel Strategies for Retirees

Retirees should set aside between 5% to 10% of their annual budget for travel. Some people dedicate up to $50,000 each year for long trips [2]. The 50/30/20 budgeting rule helps optimize spending, where travel expenses come from the 30% meant for discretionary spending [2]. Complete travel insurance becomes vital since Medicare provides limited coverage outside the United States [2].

Off-Season Travel Planning

The timing of your travels affects costs dramatically. You can save about 61% on airfare by booking flights ahead, plus $6 to $21 on hotel stays [31]. The best savings happen when you plan trips from May to early June or late August through mid-October [32]. Your trips during off-peak seasons will cost less and you’ll find fewer crowds at popular spots [2].

Maximizing Travel Rewards Programs

Travel reward credit cards give you great ways to save. Look for cards with:

- No foreign transaction fees

- Travel flexibility benefits

- Bonus points for dining and transportation

- Sign-up bonuses for new cardholders [33]

Southwest Airlines stands out with good flight rates and zero change fees, making it perfect for flexible retirement travel [33].

Balancing Travel Aspirations with Financial Reality

A detailed travel budget should include:

- Transportation costs (44% of typical travel funds) [31]

- Accommodation expenses

- Food costs (Americans spend $378 on restaurant meals versus $42 on self-prepared food while traveling) [31]

- Emergency funds for unexpected expenses [7]

Loyalty programs boost your savings potential – 43% of adults over 65 take part in travel rewards programs [31]. Longer stays of 2-3 weeks often turn out more budget-friendly [31]. Smart planning and good timing make retirement travel both fun and financially sustainable.

Implement a Tax-Efficient Retirement Strategy

Image Source: Lewis CPA

Tax planning is a vital part of making your retirement savings last longer. My experience in retirement planning shows that smart tax strategies can affect your long-term financial security by a lot.

Understanding Tax Brackets in Retirement

For 2024, single retirees face distinct tax brackets: 10% for income up to $11,600, 12% for $11,601-$47,150, and progressively higher rates reaching 37% for incomes above $609,351 [34]. Married couples filing jointly have different thresholds, starting at 10% for income up to $23,200, with brackets increasing gradually to 37% for incomes exceeding $731,201 [34].

Roth Conversion Opportunities

Roth IRA conversions from traditional retirement accounts offer unique benefits. This strategy works best between retirement and age 73, which experts call the “sweet spot” for conversions [5]. You can avoid Required Minimum Distributions (RMDs) and get tax-free withdrawals with Roth conversions, which gives you better control over future taxes [35].

Tax-Loss Harvesting in Retirement

You can reduce your investment tax burden through tax-loss harvesting. This strategy lets you offset capital gains with losses, which can reduce your taxable income by up to $3,000 each year [36]. Any extra losses roll over to future years to offset upcoming gains [37]. Note that tax-loss harvesting only applies to taxable investments, not IRAs or 401(k)s [37].

Working with Tax Professionals

Your retirement tax strategy becomes better when you work with both Certified Public Accountants (CPAs) and Certified Financial Planners (CFPs). CPAs give you expert tax planning guidance [38]. CFPs add their expertise in broader retirement strategy, which makes them valuable partners in your detailed planning [38]. These professionals help you achieve the best tax outcomes while keeping your retirement goals in focus.

These tax-efficient strategies can help you keep more of your retirement wealth. The secret is to stay flexible and review your tax situation regularly as things change [39].

Budget for Inflation Protection

Image Source: Certified Financial Planner in Los Angeles – Retire Confidently …

Retirees need proactive steps in their retirement budgets as prices keep rising. My analysis shows how inflation affects retirees and why protecting your purchasing power needs smart planning and regular tweaks.

Creating an Inflation-Adjusted Spending Plan

Inflation hit 3.4% annually in May 2024 [40]. Traditional savings accounts earning less than 1% interest don’t protect your purchasing power [40]. Your take-home pay should allocate no more than 50% toward essential expenses [41]. You should save 15% of pre-tax income for retirement and keep 5% for emergencies [41].

Investing for Inflation Protection

Stocks beat inflation historically with 10% average returns compared to 3% inflation in the last 40 years [40]. Treasury Inflation-Protected Securities (TIPS) are a great way to get extra protection by adjusting principal amounts based on Consumer Price Index changes [40]. Real estate investments typically gain value during inflationary periods because property values and rents usually rise with prices [12].

Adjusting Fixed Income for Rising Costs

Inflation needs careful management of fixed income sources. Social Security benefits include cost-of-living adjustments that offer some protection [42]. Many pension plans don’t include inflation adjustments though – a teacher’s $70,000 annual pension in 2024 stays the same in 2044, even as purchasing power drops [43].

Reviewing Budget Categories Most Affected by Inflation

Recent surveys show how inflation affects different expense categories:

- 51% of pre-retirees don’t deal very well with food and daily living costs [12]

- 45% face challenges with rising utility expenses [12]

- 78% of pre-retirees worry about their savings keeping up with inflation [12]

Skill development can boost your earning potential to handle these issues [41]. It’s worth reviewing investment costs too – inflation, taxes, and fees are the main drags on performance [41]. Your spending plan should stay flexible, with adjustments as inflation affects different budget categories in unique ways [44].

Develop a Hobby Budget That Pays for Itself

Image Source: SoFi

Retirement hobbies can do more than bring joy – they can put extra money in your pocket while making life more fulfilling. Smart planning helps these activities pay for themselves and boost your retirement budget.

Turning Passions into Supplemental Income

Many retirees have found ways to earn money from what they love doing. To cite an instance, a retired writer makes about $10,000 yearly on freelance writing platforms [45]. Some retirees earn around $1,500 monthly by pet-sitting through Rover.com [46]. Garden lovers sell their homegrown produce at farmers’ markets or through community-supported agriculture programs [47].

Affordable Ways to Start a Hobby Business

You don’t need much money to start a hobby-based business. Here are some proven ways to begin:

- Join local workshops or shared spaces to get access to tools

- Sell through Etsy, Amazon Handmade, or Fiverr to find customers

- Test the market with small batches before growing

- Look for senior discounts on supplies and memberships [48]

Smart Money Management for Hobbies

Your hobby needs careful money management to stay profitable. Put some retirement money aside each month for hobby expenses [49]. Successful hobby businesses usually start small, using skills and equipment you already have [10]. What’s interesting is that 20% of retirees started side businesses since 2020, mostly by monetizing their hobbies [9].

A smart way to handle your earnings looks like this:

- 50% goes back into growing your business and buying supplies

- 30% becomes your personal income

- 20% stays saved for unexpected costs

You’ll need proper records once you earn more than $1,000 yearly [9]. A tax professional can help you understand what hobby income means for your taxes [50]. Best of all, retirees who make money from their hobbies report feeling happier and living better lives [51].

Utilize the Envelope System for Discretionary Spending

Image Source: Albert

The envelope budgeting system gives you a great way to manage discretionary spending in retirement. My years of advising retirees show this method works well to keep your finances in check while you enjoy retirement.

Digital vs. Physical Envelope Systems

Modern smartphone apps and computer programs have transformed traditional cash-based envelope budgeting. These tools give you up-to-the-minute data analysis, better security features, and detailed spending breakdowns [52]. Digital platforms also let you instantly update spending patterns and set financial goals for smarter money management [52].

Setting Up Your Retirement Envelopes

Your first step should be analyzing spending patterns and creating specific categories. Common categories include:

- Groceries and dining

- Entertainment and hobbies

- Transportation expenses

- Personal care and clothing [11]

The most crucial part is dividing your discretionary income across these categories based on retirement lifestyle priorities. You might want to use the 50/30/20 rule, which puts 30% of your budget toward discretionary spending [53].

Adjusting Envelope Amounts Quarterly

Regular reviews help your envelope system work better. Studies show retirement spending patterns naturally shift over time, with early years showing higher discretionary expenses [54]. So you should adjust envelope amounts based on:

- Seasonal spending variations

- Changes in retirement activities

- Healthcare needs

- Travel plans [55]

Psychology of Cash Spending in Retirement

Research shows people who use physical cash feel more connected to their money and spend less than credit card users [53]. The envelope system helps prevent overspending because it creates clear boundaries for each expense category [56]. This approach works especially well for retirees who switch from regular paychecks to fixed income sources [57].

You can gain better control over discretionary spending while keeping financial flexibility by using either digital or traditional envelope budgeting. Start with a few key categories and expand gradually as you get comfortable with the system [52].

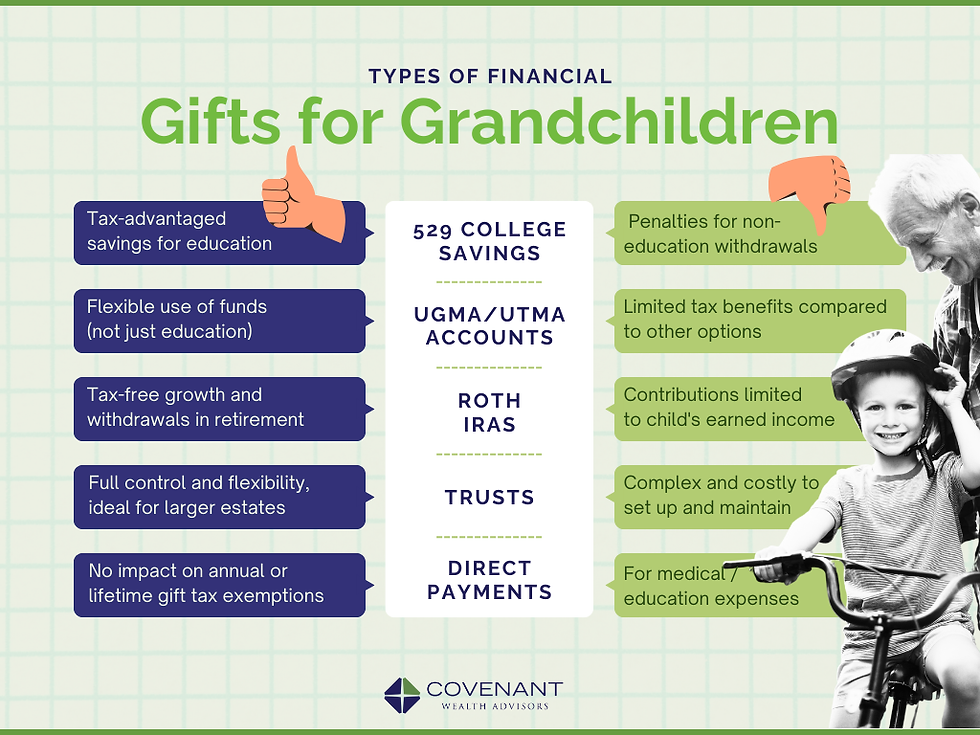

Plan for Multi-Generational Financial Support

Image Source: Covenant Wealth Advisors

Supporting family members financially takes careful planning in retirement. My years of advising retirees have shown that clear guidelines are vital to stay generous while keeping your financial security intact.

Setting Boundaries for Family Financial Assistance

Living with multiple generations under one roof calls for thoughtful money boundaries. Recent data shows that 62% of people aged 50 and above help their family members financially [58]. You retain control and keep relationships healthy by setting clear guidelines from the start:

- Put firm end dates on temporary help

- Spell out what each person contributes

- Write down loan terms and when they’ll be paid back

- Put shared living arrangements in writing [59]

Creating a Family Support Fund

A dedicated emergency fund makes unexpected family expenses easier to handle. You should keep three to six months of household costs in an available account [60]. Just don’t park too much money in low-interest emergency funds. Once you hit your target, put extra money into tax-advantaged investments or high-yield savings [60].

Tax-Efficient Gifting Strategies

By 2025, you can give up to $19,000 yearly to each person without tax consequences [61]. Couples can jointly give $38,000 to each recipient [61]. If you want to help with education, here are smart options:

- Put money in 529 college savings plans

- Pay tuition straight to schools

- Set up health savings accounts for medical costs [60]

Balancing Generosity with Self-Care

Your financial stability comes first when helping family members. Studies show that all but one of these caregivers stop working to provide care [62]. Caregivers typically spend $7,200 yearly to support their families [62]. Here’s what works best:

- First assess what you’ll need in retirement

- Talk to financial advisors before making big gifts

- Look over support arrangements every three months

- Be upfront about your financial limits [59]

Note that helping family shouldn’t put your retirement at risk. Working with money professionals helps you create lasting support plans while protecting your long-term financial health [63].

Implement a Quarterly Budget Review Process

Image Source: FasterCapital

Financial check-ups are the life-blood of successful retirement planning. My expertise in retirement budgeting shows that quarterly reviews play a vital role to maintain financial health and adapt to changing circumstances.

Evaluating Budget Performance

Your quarterly review should start with a comparison of income and expenses against projected targets [64]. The process helps you track spending patterns, spot trends, and measure progress toward financial goals [64]. This approach catches problems early and lets you make timely adjustments before small issues become major challenges [3].

Making Seasonal Adjustments

Budget management needs flexibility to handle seasonal variations. Cash flow patterns can be uneven and need careful planning, especially when expenses change throughout the year [65]. Here are the adjustments to think about:

- Cut back spending in slower periods

- Save more during peak income months

- Keep spending minimal during off-seasons [65]

Incorporating Life Changes into Your Budget

Your budget must adapt as life changes happen. Recent data reveals that 31% of retirees spend more than they plan [66], which makes regular reviews vital. Healthcare costs rise faster than other expenses, so your budget needs periodic updates [67]. Living expenses might drop when children move out, but travel costs often climb because of family visits [67].

Working with a Financial Advisor

Expert guidance improves the effectiveness of retirement planning. A financial advisor helps develop strategies that adjust to market changes [68]. They give valuable guidance about:

- Cash flow planning through retirement phases

- Testing plans against market conditions

- Building sustainable withdrawal strategies

- Organizing portfolios for different time periods [69]

A full quarterly review takes about 15 minutes once you have all documents ready [3]. The process should focus on savings progress, investment performance, and insurance coverage [3]. You should also calculate your net worth by subtracting debts from assets to see your financial position clearly [3]. These regular reviews help you stay on top of your retirement finances and feel confident about your long-term planning decisions [70].

Create a Legacy and Estate Planning Budget

Image Source: BCR Wealth Strategies

Estate planning plays a vital part in your retirement financial strategy. My experience with retirees shows that smart budgeting for legacy planning will give your assets the best chance to benefit future generations.

Budgeting for Estate Planning Services

Simple estate planning costs range from $1,200 to $4,000 for complete documentation [1]. Key services include wills, trusts, and power of attorney documents. Estates with businesses might need $4,000 to $5,000 [1]. Standard documents come under flat-fee plans, while specialized needs cost between $200 to $500 per hour [1].

Charitable Giving Strategies

Retirement account charitable donations provide excellent tax benefits. You can bypass income taxes through direct IRA contributions to charities while meeting Required Minimum Distributions [71]. Donor-advised funds let you contribute now for immediate tax benefits and distribute donations later [71]. Charitable gift annuities also provide guaranteed lifetime income and tax deductions [72].

Creating a Legacy Fund

Your dedicated legacy funds need careful asset type selection. Life insurance policies work well as versatile tools, especially when you have estate taxes to consider [13]. Strategic planning becomes vital with the 2025 federal estate tax exemption at $13.99 million per individual [13]. Here’s what you should do:

- Keep beneficiary designations current

- Check trust funding timelines

- Align tax strategies across retirement accounts

Tax-Efficient Inheritance Planning

Asset allocation substantially affects inheritance taxes. Heirs pay ordinary income tax on inherited traditional retirement accounts, unlike other tax-free inherited assets [71]. Smart Roth conversions can reduce tax burdens for beneficiaries [13]. Trusts that are five years old before long-term care needs can protect assets effectively [13].

Your retirement budget should include all these elements to create a lasting financial legacy. Working with estate planning attorneys helps you stay compliant with current regulations [73]. Good coordination between retirement and estate planning secures your future and your beneficiaries’ inheritance [74].

Comparison Table

| Budget Tip | Main Goal/Purpose | Key Financial Effect | Implementation Timeline | Notable Statistics/Data |

|---|---|---|---|---|

| Create a Retirement Budget Baseline | Build foundation for retirement spending | 54-87% of pre-retirement income needed | Before retirement | Average retiree needs $54,975 yearly for household expenses |

| Match Fixed Expenses to Guaranteed Income | Line up core costs with reliable income sources | Covers living expenses | Pre-retirement planning | 73% of Americans use Social Security for monthly costs |

| Implement 4% Withdrawal Rule | Green retirement fund withdrawal | 3.7% recommended starting rate for 2025 | Throughout retirement | Success rate rises from 36% to 56% with dynamic strategy |

| Budget for Healthcare (Three-Tier) | Handle medical expenses systematically | $330,000 for average retired couple | Age 65+ | Private nursing home costs: $10,025 monthly |

| Automate Bill Payments and Savings | Make financial management easier | Cuts fees and missed payments | Immediate implementation | Electronic payments cost 8x less than checks |

| Adopt Go-Go, Slow-Go, No-Go Framework | Smart retirement spending by phase | Drops 2% yearly in later phases | Three distinct phases | Healthcare becomes main expense in No-Go phase |

| Combine Financial Accounts | Make account management easier | Cuts fees and admin costs | Pre-RMD age (before 73) | RMDs begin at age 73 |

| Create Green Travel Budget | Match travel wishes with resources | 5-10% of yearly budget | Early retirement years | Up to $50,000 yearly for extensive travel |

| Implement Tax-Efficient Strategy | Lower tax liability | Varies by tax bracket | Ongoing | 2024 tax brackets start at 10% for income up to $11,600 |

| Budget for Inflation Protection | Keep purchasing power | 3.4% yearly inflation rate (2024) | Regular monitoring | 78% of pre-retirees worry about inflation effects |

| Develop Hobby Budget | Create extra income | $1,500+ monthly potential | Flexible | 20% of retirees started side ventures since 2020 |

| Use Envelope System | Manage fun spending | 30% of budget for extras | Monthly allocation | Based on 50/30/20 rule |

| Plan Multi-Generational Support | Handle family money help | $7,200 yearly average support cost | Ongoing | 62% of people over 50 help family financially |

| Implement Quarterly Reviews | Regular money checkups | Varies by person | Every 3 months | 31% of retirees spend too much |

| Create Legacy Planning Budget | Estate and inheritance planning | $1,200-$4,000 simple planning costs | 5+ years before need | 2025 estate tax exemption: $13.99 million |

Conclusion

Successful retirement budgeting needs attention to several financial aspects. My experience shows that retirees become skilled at these 15 budget strategies when they implement them consistently and adjust them regularly.

Retirement planning works best with a tailored approach. Your unique circumstances and goals should shape each strategy – from matching fixed expenses with guaranteed income to creating travel budgets you can maintain. A retired couple who spends $330,000 on healthcare needs different allocations compared to someone focused on legacy planning with a $13.99 million estate tax exemption.

Your retirement budget baseline serves as the starting point. You can build on this foundation when you implement automated systems, conduct quarterly reviews, and adjust for inflation. My clients who take this well-laid-out approach feel more confident about their retirement security and make spending decisions freely.

A secure retirement comes from planning ahead and making smart adjustments. You can learn about more retirement planning and get practical financial advice at trendnovaworld.com. Note that retirement budgeting isn’t about limiting yourself – it creates a lasting framework that supports your lifestyle while protecting your financial future.

More Insights Await! Explore These Top Reads:

• 🏠 How to Master Working from Home – Entrepreneurs Are Winning in 2025 (Real Data Inside)

• 🤖 Mastering Fully Automated Websites – My 2025 Experience

• 🎨 My Top UI/UX Design Tools for AR & VR Interfaces in 2025

• 🌐 Discover the Best Web Hosting for Your AI-Powered Website in 2025

FAQs

Q1. How much should I budget for retirement travel? Experts recommend allocating 5-10% of your annual retirement budget for travel expenses. Some retirees dedicate up to $50,000 annually for extensive journeys. Consider using the 50/30/20 budgeting rule, where travel falls under the 30% allocated for discretionary spending.

Q2. What is the “Go-Go, Slow-Go, No-Go” retirement budget framework? This framework divides retirement into three phases: “Go-Go” (early, active years), “Slow-Go” (mid-retirement with decreased activity), and “No-Go” (later years with increased healthcare needs). Spending typically declines by about 2% annually during the Slow-Go phase, while healthcare becomes the primary expense in the No-Go phase.

Q3. How can I protect my retirement savings from inflation? To combat inflation, consider investing in stocks, which historically outperform inflation with 10% average returns compared to 3% inflation over the past 40 years. Additionally, explore Treasury Inflation-Protected Securities (TIPS) and real estate investments, which often appreciate during inflationary periods.

Q4. What’s the recommended withdrawal rate from retirement savings? While the traditional 4% rule has been a common guideline, recent analysis suggests a 3.7% starting withdrawal rate for 2025 to ensure your retirement savings last through a 30-year retirement. Implement a dynamic withdrawal strategy, adjusting based on market performance to potentially increase your success rate from 36% to 56%.

Q5. How much should I budget for healthcare expenses in retirement? An average retired couple should set aside approximately $330,000 for medical expenses throughout retirement, excluding long-term care. Budget for routine medical costs, chronic condition management, and potential catastrophic health events. Consider that private nursing home care can cost around $10,025 monthly, while assisted living facilities average $5,511 per month.

References

[1] – https://www.kiplinger.com/retirement/retirement-planning/how-to-save-money-on-estate-planning

[2] – https://finance.yahoo.com/news/12-ways-travel-retirement-without-170120919.html

[3] – https://www.getevolved.com/customer-care/resource-center/improve-your-financial-health/financial-checklist-heres-what-to-review-each-quarter/

[4] – https://www.pfbt.com/emerging-technological-innovations-in-the-401k-retirement-industry

[5] – https://www.investopedia.com/ask/answers/030316/do-retirement-account-withdrawals-affect-tax-brackets.asp

[6] – https://slavic401k.com/the-role-of-technology-in-retirement-planning-tools-and-trends/

[7] – https://annuity.com/retirement-planning/creating-a-retirement-plan-that-includes-travel/

[8] – https://thefiscalfemme.com/articles/simplify-your-banking

[9] – https://taking.care/blogs/resources-advice/retirement-hobbies-that-make-money?srsltid=AfmBOooyilXnsBWHfWN8LViSvgB3G81DcYQxAjBTefgMO49ZpkMZ9Eqj

[10] – https://www.business.com/articles/how-make-money-retirement-hobby/

[11] – https://www.dfcu.com/articles/envelope-budgeting-cash-vs-digital/

[12] – https://www.kiplinger.com/retirement/how-to-help-shield-your-retirement-from-inflation

[13] – https://www.kiplinger.com/retirement/how-estate-planning-can-make-your-retirement-easier

[14] – https://www.kiplinger.com/retirement/ways-to-prepare-for-long-term-care-expenses-in-retirement

[15] – https://www.bankerslife.com/insights/life-events/8-things-you-need-to-consider-when-it-comes-to-long-term-care/

[16] – https://www.opm.gov/retirement-center/how-to-make-a-payment/

[17] – https://www.bankrate.com/banking/savings/grow-your-savings-with-automatic-transfers/

[18] – https://www.eastrise.com/blog/ten-ways-automatic-transfers-help-you-save-more-money/

[19] – https://401kspecialistmag.com/1-in-3-guilty-of-overspending-in-retirement-ebri/

[20] – https://www.truist.com/money-mindset/principles/budgeting-by-values/avoid-overdrafts-with-low-balance-alerts

[21] – https://www.pnc.com/insights/personal-finance/invest/automatic-savings-plan-tips.html

[22] – https://www.ml.com/articles/planning-for-stages-of-retirement.html

[23] – https://www.nasdaq.com/articles/go-go-slow-go-and-no-go-years:-how-to-create-a-budget-for-each-retirement-phase

[24] – https://www.kiplinger.com/retirement/plan-for-retirement-go-go-slow-go-and-no-go-years

[25] – https://www.pranawealth.com/three-phases-of-retirement-how-your-spending-changes/

[26] – https://retirable.com/advice/income/budgeting-for-the-four-financial-phases-of-retirement

[27] – https://investor.vanguard.com/investor-resources-education/retirement/savings-retirement-accounts

[28] – https://www.planmember.com/ifs/consolidating-retirement-accounts/

[29] – https://smartasset.com/retirement/how-to-choose-an-ira-account

[30] – https://www.fidelity.com/building-savings/advantages-of-consolidating-accounts

[31] – https://secondwindmovement.com/retirement-travel-on-a-budget/

[32] – https://www.athene.com/smart-strategies/easy-ways-to-rack-up-travel-rewards.html

[33] – https://www.nerdwallet.com/article/travel/simple-ways-retirees-can-earn-travel-rewards

[34] – https://www.thrivent.com/insights/taxes/taxes-in-retirement-a-comprehensive-guide

[35] – https://investor.vanguard.com/investor-resources-education/iras/ira-roth-conversion

[36] – https://www.forbes.com/sites/andrewrosen/2024/05/09/tax-loss-harvesting-and-your-retirement/

[37] – https://turbotax.intuit.com/tax-tips/investments-and-taxes/5-situations-to-consider-tax-loss-harvesting/L06jlQWfl

[38] – https://money.usnews.com/money/retirement/iras/articles/should-you-consult-cfp-or-cpa-to-plan-for-retirement

[39] – https://investor.vanguard.com/advice/tax-efficient-retirement-strategy

[40] – https://www.bankrate.com/retirement/how-to-keep-inflation-from-wrecking-retirement/

[41] – https://www.fidelity.com/learning-center/personal-finance/retirement/saving-for-retirement-and-inflation

[42] – https://www.fidelity.com/learning-center/personal-finance/retirement/inflation-retirement-income

[43] – https://www.fuchsfinancial.com/learning-center-post/inflation-in-retirement/

[44] – https://www.getsmarteraboutmoney.ca/learning-path/budgeting/inflation-and-your-household-budget/

[45] – https://www.athene.com/smart-strategies/turn-your-passion-into-retirement-income.html

[46] – https://www.forbes.com/sites/nextavenue/2017/08/28/how-to-turn-your-passions-into-retirement-income/

[47] – https://www.investopedia.com/retirees-make-money-from-hobbies-11680775

[48] – https://www.tcdrs.org/library/how-to-fund-your-retirement-hobby/

[49] – https://www.suncanyon.bank/blog/post/starting-a-new-hobby-in-retirement-exploring-interesting-and-affordable-options

[50] – https://blog.massmutual.com/retiring-investing/retirement-activities-hobbies

[51] – https://www.terrabellaseniorliving.com/senior-living-blog/turning-passion-into-profit-7-money-making-hobbies-for-retirement/

[52] – https://m1.com/knowledge-bank/digital-envelope-system/

[53] – https://www.nerdwallet.com/article/finance/envelope-system

[54] – https://www.raymondjames.com/manhattan-branch/commentary-and-insights/2024/10/22/the-psychological-side-of-spending-your-retirement-savings

[55] – https://www.cnn.com/2022/10/03/business/money/spending-savings-in-retirement-psychological-adjustment/index.html

[56] – https://www.quorumfcu.org/learn/money-management/the-digital-envelope-budgeting-system/

[57] – https://finance.yahoo.com/news/psychology-retirement-income-saving-spending-191724081.html

[58] – https://paxfinancialgroup.com/financial-planning/10-ways-to-support-family-members-without-risking-your-retirement/

[59] – https://www.northwesternmutual.com/life-and-money/5-ways-to-set-boundaries-if-youre-providing-financial-support-to-adult-children/

[60] – https://www.usbank.com/financialiq/plan-your-future/manage-wealth/multigenerational-household-financial-planning-strategies.html

[61] – https://www.fidelity.com/viewpoints/wealth-management/insights/lifetime-gifting

[62] – https://www.ncoa.org/article/finding-financial-assistance-for-family-caregivers/

[63] – https://www.fortpittcapital.com/blog/how-does-multigenerational-planning-work/

[64] – https://www.financestrategists.com/financial-advisor/financial-planning/quarterly-review/

[65] – https://www.stillmanbank.com/finance/how-to-budget-when-you-have-seasonal-income/

[66] – https://www.journalofaccountancy.com/issues/2024/feb/preparing-clients-for-lifestyle-changes-in-retirement.html

[67] – https://www.schwab.com/learn/story/retirement-budget-planning-9-steps-to-consider

[68] – https://www.securian.com/insights-tools/articles/retirement-budget-tips.html

[69] – https://manual.compoundplanning.com/chapters/how-to-embrace-a-spenders-mindset-in-retirement

[70] – https://threebearings.com/you-should-know/articles/retirement_income_planning.cfm

[71] – https://www.fidelitycharitable.org/guidance/philanthropy/donating-retirement-assets-to-charity.html

[72] – https://www.kiplinger.com/retirement/5-tax-smart-charitable-giving-strategies-for-retirees

[73] – https://www.intelligentinvestment.com/blog-01/estate-planning-retirement-protecting-your-legacy

[74] – https://frankkraft.com/how-retirement-planning-and-estate-planning-work-together/